- Mongabay has begun publishing a new edition of the book, “A Perfect Storm in the Amazon,” in short installments and in three languages: Spanish, English and Portuguese.

- Author Timothy J. Killeen is an academic and expert who, since the 1980s, has studied the rainforests of Brazil and Bolivia, where he lived for more than 35 years.

- Chronicling the efforts of nine Amazonian countries to curb deforestation, this edition provides an overview of the topics most relevant to the conservation of the region’s biodiversity, ecosystem services and Indigenous cultures, as well as a description of the conventional and sustainable development models that are vying for space within the regional economy.

- Click the “A Perfect Storm in the Amazon” link atop this page to see chapters 1-13 as they are published during 2023 and 2024.

Palm oil is different from most agricultural commodities because the raw harvested product, fresh fruit bunches, must be processed within 48 hours or it will spoil. This fact dictates that plantations and mills must be in close juxtaposition. In the case of soy and beef, the decision on where to locate a crushing mill or slaughterhouse is an option with considerable leeway, and its existence is not a prerequisite to the installation of a production system. In contrast, palm oil is a hundred per cent dependent upon the simultaneous creation of a mill and a plantation at the initiation of the development process.

Palm oil mills require a significant capital investment and a large-scale facility capable of competing in the global market requires an investment of about US$ 40 million. To justify this capital outlay, institutional investors require that the mill be accompanied by a plantation of at least 5,000 hectares (12,355 acres) to ensure the supply of sufficient feedstock to safeguard the viability of the mill. At about US$ 10,000 per hectare, a 5,000-hectare plantation would require another US$ 50 millions of investment capital.

Oil palm is cultivated for two basic products: palm oil, which is extracted from the fruit, and palm kernel oil, which is extracted from the seeds. Palm oil is used in products ranging from cooking oil and ice cream to soap and toothpaste and is a feedstock for the biofuel and chemical industries. Palm kernel oil is similar to coconut oil and enjoys a market niche linked to cosmetics and personal care products.

Thirty years ago, palm oil represented less than two per cent of global consumption of fats and oils; today that figure stands at 41 per cent. In 2020, the cultivated extent of oil palm reached 28 million hectares (69 million acres) globally, with an annual growth rate of 5.5 % between 2000 and 2020, more than double the annual growth rate of soybeans (2.6 %). Palm oil displaced soy as the world’s most important vegetable oil in 2006. Its dominance as a feedstock for the consumer goods industry is due to its lower cost of production versus soy oil and the chemical characteristics of its constituent fatty acids, which make it a more attractive ingredient for many recipes and formulas.

Global supply chains for palm oil are dominated by producers from Southeast Asia because they have created a hyper-efficient production system based on access to state lands, low labor costs and strategic investments in technology and management systems. Producers in Latin America have missed out on this spectacular growth because their costs of production are significantly higher than their competitors in Indonesia and Malaysia. According to a recent study, the total cost per tonne of crude palm oil produced by an integrated Colombian or Brazilian producer was approximately double that incurred by similar companies in Southeast Asia.

The difference was due largely to higher labor costs, but efficiency and superior yields also favor Southeast Asian producers. The cost differential makes it difficult for South American producers to compete in international markets and forces them to accept lower profit margins. This has caused them to focus on domestic markets, at least in the early stages of their development, but most companies are now focusing on export markets as a growth strategy.

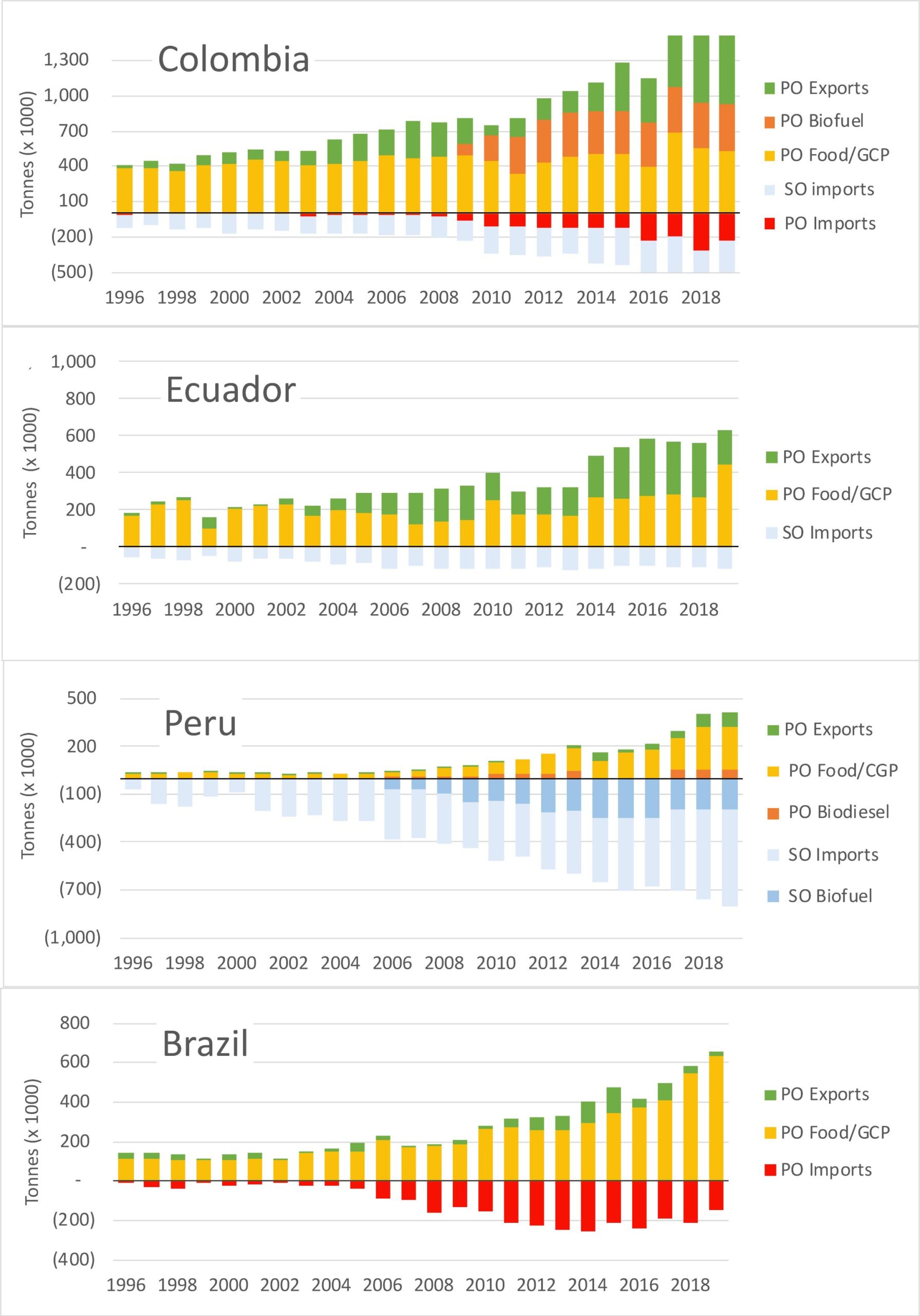

Each country has pursued different development strategies, which has influenced how rapidly they have expanded and their ability to compete in national and global markets.

Colombian producers were making progress in penetrating overseas markets, but a disease outbreak in 2010 combined with drought conditions limited gains at the time when the sector was increasing plantation area in response to a national biofuel policy. The biofuel policy did promote the expansion of the industry and enabled the sector to export greater quantities overseas.

Ecuador has a similar history, including periodic bouts with plant pathogens but, unlike Colombia, Ecuador’s government did not embrace a biodiesel policy. Consequently, the palm oil sector has expanded by focusing exclusively on exports. Domestic consumption in both Colombia and Ecuador is flat; major export markets include Venezuela, the EU, Mexico, Chile and Brazil. Ecuador actually exports about thirty per cent of its production to Colombia.

Peruvian producers have not only failed to garner a significant export market but have also failed to reduce the country’s dependence on imported soy oil. The macroeconomic incentives for expanding palm oil production in Peru would seem obvious to a casual observer since it would replace imported soy oil. The expansion of oil palm plantations in Peru is increasing and will be a significant driver of land-use change in Amazonian Peru over the medium term.

Brazil has enjoyed consistent growth of its palm oil sector, but domestic demand has far outpaced the ability of producers to meet supply. Brazil is the world’s second-largest producer of soybeans, so palm oil must compete with soy oil for market share. For example, Brazil has a long-established policy of using biofuels as alternative energy sources, but very little palm oil has been allocated to the biodiesel market.

Brazil has a massive market for consumer goods, and many global brands manufacture their products in Brazil using derivatives from palm oil or palm kernel oil. Apparently, the lack of domestic production combined with cheaper imports has motivated companies to source between twenty and forty per cent of Brazilian demand from overseas suppliers. Colombian and Ecuadorian imports represent about ten per cent of total imports, so the remainder must be coming from Southeast Asia.

The future Brazilian market for palm oil may be at a crossroads. The 100,000 hectares (247,105 acres) of new plantations established in Pará between 2010 and 2016 were intended originally to be used as feedstocks in an expanding biofuel industry, either for export to the EU (Belem Bioenergia Brasil) or to defray the cost of diesel consumed by Vale’s heavy machinery and railroad operations (Biopalma da Amazônia).

However, the decline in demand for biodiesel may change this calculus, and this new production – which has yet to come fully online – might be targeted at Brazil’s expanding consumption of traditional uses of palm oil.

Over the short term, there is considerable uncertainty regarding the future of the palm oil sector in the Pan Amazon. Production in Ecuador and Peru will probably continue to expand, but almost all this expansion will occur via smallholders and independent producers. In Colombia, the current government has changed the biofuel policies that contributed to the expansion of the sector over the last decade, but a decline in domestic demand may be offset by increasing exports. Brazil has almost unlimited capacity for expansion, and government policy in the recent past has favored the sector; however, recent expansion may have saturated domestic demand for the next several years.

In all four countries, expansion will occur without deforestation by large-scale producers due to market pressure. Some small-scale deforestation will occur in Ecuador and Peru because smallholders are not subject to the same level of monitoring. That forest loss will occur via the loss of forest remnants or the gradual expansion of the agricultural frontier.

“A Perfect Storm in the Amazon” is a book by Timothy Killeen and contains the author’s viewpoints and analysis. The second edition was published by The White Horse in 2021, under the terms of a Creative Commons license (CC BY 4.0 license).

Read the other excerpted portions of chapter 3 here:

Chapter 3. Agriculture: Profitability determines land use

-

- Agriculture: profitability determines land use October 10, 2023

- Agriculture in the Pan Amazon: Beef production models October 11, 2023

- Industrial infrastructure in the Pan Amazon October 17, 2023

- National versus global markets – beef in the Brazilian Amazon October 19, 2023

- Livestock farming in the Andean Amazon and the rest of the Amazon October 24, 2023

- Intensive agriculture in the Pan Amazon: Soy, maize and other field crops October 25, 2023

- Agriculture in the Pan Amazon: Global markets for soybean and corn crops October 31, 2023

- Agriculture in the Pan Amazon: Industrial infrastructure for grains and cereals November 1, 2023

- Agriculture in the Pan-Amazon: Swine and poultry – Adding value to farm production November 8, 2023

- Oil palm in the Pan Amazon November 9, 2023

- Palm oil cultivation in Colombia, Ecuador, Peru and Brazil November 13, 2023

- What does oil palm require to reach international markets? November 14, 2023

- Biofuels in the Pan Amazon November 21, 2023

- Coffee and cacao in the Pan Amazon November 22, 2023

- Cultivation and processing of Amazonian coffees November 28, 2023

- High quality cacao in Amazonia November 29, 2023

- Local and national food crops in the Andean Amazon December 5, 2023

- Coca in the Amazon – The anti-development crop December 6, 2023