Beijing Tiandi Riyue Biomass Technology Corp. Ltd. has started construction on its new fuel ethanol project in the county of Naiman in Inner Mongolia Autonomous Region's Chifeng City, the company's president told Interfax today.

Beijing Tiandi Riyue Biomass Technology Corp. Ltd. has started construction on its new fuel ethanol project in the county of Naiman in Inner Mongolia Autonomous Region's Chifeng City, the company's president told Interfax today.

World Oil Outlook 2007: high prices to stay, biofuels may erode OPEC oil demand

The Organisation of Petroleum Exporting Countries (OPEC) has released its World Oil Outlook 2007 [*.pdf], which contains some interesting perspectives for biofuels, tightly linked to the way OPEC will invest in future capacity expansion.

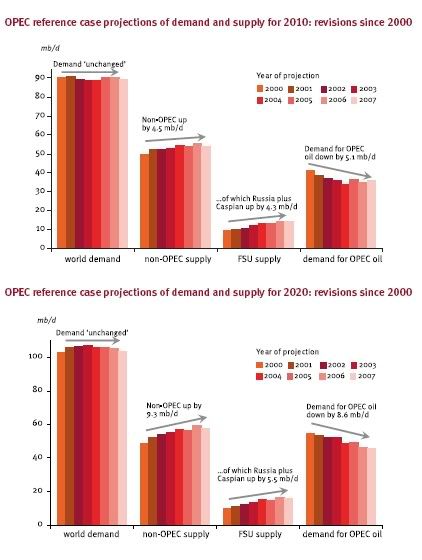

Most importantly, according to the report, the demand for OPEC crude by 2010 has been revised downwards and will be almost 1 million barrels per day (mb/d) below 2005 levels because of the rise of non-OPEC non-conventional resources (including biofuels) (click to enlarge). Thereafter, demand for OPEC oil will gradually increase. But uncertainties over demand, driven by the rise of green fuels and non-conventional resources, may have serious consequences and delay much needed investments across the entire supply chain. Especially the addition of new oil refinery capacity may get delayed.

Most importantly, according to the report, the demand for OPEC crude by 2010 has been revised downwards and will be almost 1 million barrels per day (mb/d) below 2005 levels because of the rise of non-OPEC non-conventional resources (including biofuels) (click to enlarge). Thereafter, demand for OPEC oil will gradually increase. But uncertainties over demand, driven by the rise of green fuels and non-conventional resources, may have serious consequences and delay much needed investments across the entire supply chain. Especially the addition of new oil refinery capacity may get delayed.

However, if the ambitious biofuel targets in the OECD are not met, the result could be further tightness in the downstream, and possibly the upstream, and in turn, this could have a significant impact on prices, margins and volatility. Such an event would automatically kickstart biofuel production again.

Global outlook

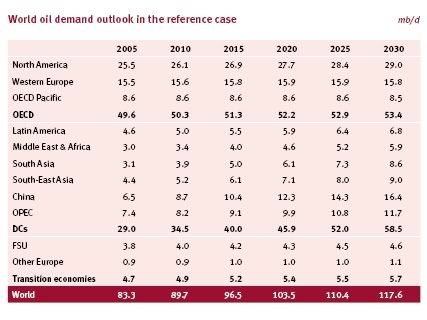

According to the report demand for energy in general is set to continue to grow (click to enlarge) and oil is expected to maintain its leading position in meeting the world’s growing energy needs for the foreseeable future. In OPEC's reference case, with an average global economic growth rate of 3.5% per annum (purchasing power parity basis), and oil prices assumed to remain in the $50-60/b range in nominal terms for much of the projection period, oil demand is set to rise from the 2005 level of 83 mb/d to 118 mb/d by 2030.

According to the report demand for energy in general is set to continue to grow (click to enlarge) and oil is expected to maintain its leading position in meeting the world’s growing energy needs for the foreseeable future. In OPEC's reference case, with an average global economic growth rate of 3.5% per annum (purchasing power parity basis), and oil prices assumed to remain in the $50-60/b range in nominal terms for much of the projection period, oil demand is set to rise from the 2005 level of 83 mb/d to 118 mb/d by 2030.

This assumes that no particular departure in trends for energy policies and technologies takes place. This is a very important caveat for there are inherent downside risks to demand, something that is specifically addressed in the Outlook. One of these 'risks', is indeed the fast growth of biofuels and non-OPEC, non-conventional oil resources.

OECD countries, currently accounting for close to 60% of world oil demand, see a further growth of 4 mb/d by 2030, reaching 53 mb/d - mainly coming from North America. Developing countries account for most of the rise in the reference case, with consumption doubling from 29 mb/d to 58 mb/d. Asian developing countries account for an increase of 20 mb/d, which represents more than two-thirds of the growth in all developing countries.

Nevertheless, the Outlook assumes that energy poverty will remain an important issue over this period. By 2030, developing countries will consume, on average, approximately five times less oil per person, compared with OECD countries.

Demand per sector

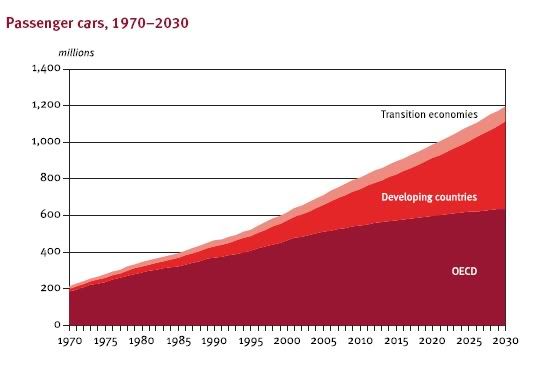

The transportation sector will be the main source of future oil demand increases. Growth in the OECD is expected to continue to rise, although saturation effects should increasingly have an impact upon the growth in passenger car ownership. The potential for growth in the stock of cars, buses and lorries, however, is far greater in developing countries (click to enlarge). For example, two-thirds of the world’s population currently live in countries with less than one car per 20 people. The total stock of cars is expected to rise from 700 million in 2005 to 1.2 billion by 2030, and the global volume of commercial vehicles is anticipated to more than double:

The transportation sector will be the main source of future oil demand increases. Growth in the OECD is expected to continue to rise, although saturation effects should increasingly have an impact upon the growth in passenger car ownership. The potential for growth in the stock of cars, buses and lorries, however, is far greater in developing countries (click to enlarge). For example, two-thirds of the world’s population currently live in countries with less than one car per 20 people. The total stock of cars is expected to rise from 700 million in 2005 to 1.2 billion by 2030, and the global volume of commercial vehicles is anticipated to more than double:

biofuels :: energy :: sustainability :: ethanol :: biodiesel :: biomass :: petroleum :: oil :: OPEC ::

biofuels :: energy :: sustainability :: ethanol :: biodiesel :: biomass :: petroleum :: oil :: OPEC ::

Of the non-transportation oil use, the main expected source of increase will be in

the industrial and residential sectors of developing countries, which see a combined

growth to 2030 of over 11 mboe/d in the reference case. Oil use in households is closely associated with the gradual switch away from traditional fuels. This trend is expected to continue, especially in the poorer developing countries of Asia and Africa, with the urbanisation movement throughout the developing world central to the shift towards commercial energy.

Despite the expected continued growth in electricity production and consumption, oil demand in this sector will experience no significant growth.

No 'Peak Oil', Non-OPEC production plateau

Resources are sufficient to meet future demand. Estimates from the US Geological

Survey of ultimately recoverable reserves have doubled since the early 1980s, while

cumulative production during this period was less than one-third of this increase.

This has been due to such factors as technology, successful exploration and enhanced

recovery from existing fields. On top of this, there is a vast resource base of nonconventional oil to explore and develop.

Non-OPEC crude oil supply at first rises in the reference case to a plateau of around 48 mb/d, before beginning a gradual decline from around 2020. This plateau is initially maintained as increases from Latin America (chiefly Brazil), Russia and the Caspian compensate for decreases elsewhere, mainly in the North Sea. The Middle East

and Africa region experiences a slight rise in volumes over the medium-term to 2010,

but this reaches a plateau of close to 5 mb/d. Non-OPEC crude oil supply is expected

to be just over 45 mb/d in 2030.

Biofuels, non-conventional oil

Regarding non-conventional oil supply and biofuels from non-OPEC countries, the most significant growth is expected to come from the Canadian oil sands, which is seen rising in the reference case to 5 mb/d in 2030, from just 1 mb/d in 2005. Coal-to- liquids and gas-to-liquids are also expected to grow, from about 150,000 b/d and less than 50,000 b/d, to 1.5 mb/d and 500,000 b/d respectively from 2005–2030. These increases will come predominantly from the US, China, South Africa and Australia.

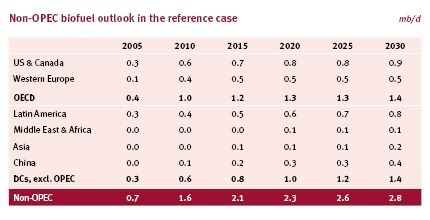

The use of biofuels is also increasing in many regions throughout the world, and recent pronouncements of ambitious targets amplify uncertainties for future demand and supply volumes. In total, the reference case sees more than 10 mb/d of nonconventional oil supply including biofuels coming from non-OPEC by 2030, 8 mb/d more than in 2005.

Of those 10 mb/d, the bulk may come from biofuels, under a high scenario:

Uncertainty over the magnitude of the rise in non-OPEC non-conventional supply is growing. For example, the European Union recently adopted a minimum binding target for biofuels to reach a 10% share in transport gasoline and diesel consumption.

Uncertainty over the magnitude of the rise in non-OPEC non-conventional supply is growing. For example, the European Union recently adopted a minimum binding target for biofuels to reach a 10% share in transport gasoline and diesel consumption.

And in the US, the most recent proposal, as reflected in the ‘Twenty In Ten Goal’, proposes alternative transport fuels hitting over 2 mb/d by 2017.

The Outlook's reference scenario for biofuel supply is extremely conservative (click to enlarge) compared to projections by other organisations (such as the IEA) or to the cumulative supply that would emerge if actual targets set by countries are met. But even in this reference case, OPEC sees the rise of biofuels as an important factor in the uncertainty over OPEC oil demand.

Demand for OPEC crude falls, stabilize, falls

Initial increases in both crude and non-crude supply pushes total non-OPEC supply up to 54 mb/d in 2010. This is 5 mb/d higher than in 2005. With demand rising by only a slightly higher rate, this leaves little room for additional OPEC oil. Indeed, with OPEC non-crude supply, primarily natural gas liquids (NGLs), set to rise to just under 6 mb/d by 2010, the demand for OPEC crude by 2010 is almost 1 mb/d below 2005 levels.

After 2010, non-OPEC crude supply, including NGLs, stabilises, then eventually falls. Yet with non-conventional oil supply increasing at strong rates, over the entire projection period, total non-OPEC supply actually continues to rise. The amount of

crude oil supply expected from OPEC increases post-2010, rising, in this reference case, to 38 mb/d by 2020 and 49 mb/d by 2030.

Investments in capacity

These projections underline the need for substantial investment along the entire supply chain. Expansion of non-OPEC capacity is two-to-three times more costly than in OPEC, with this gap widening over time. The highest cost region is the OECD, which also experiences the highest decline rates. Up to 2030, total upstream investment requirements, from 2006 onwards, amount to $2.4 trillion (in 2006 US$).

These estimates, however, do not include necessary infrastructure investments. Concerning crude oil price assumptions for medium- to long-term analyses, it has been observed that the oil industry, guided by the recent price trends, has mostly revised upward the business-as-usual price assumptions. A further observation is that, due to the effect of several factors, economic growth and oil demand are both now more resilient to higher oil prices than had previously been thought.

All these trends, in addition to rising costs, have become integral to the general perception of higher expected prices in the long-term. Continuous downward revisions to demand projections from organizations such as the International Energy Agency and the US Department of Energy/Energy Information Administration are also noted. In this regard, a key question is whether this downward revision process is set to continue.

On the supply side, there has been a steady rise in expectations for non-OPEC production in the longer term. Increased attention is being paid to non-conventional oil and biofuels and a discernibly higher expected contribution to supply is emerging.

Uncertainty over demand

There is a great deal of uncertainty over future demand and non-OPEC supply, which translates into large uncertainties over the amount of oil that OPEC Member Countries will eventually need to supply. Investment requirements are very large, and subject to considerably long lead-times and pay-back periods. It is therefore essential to explore these uncertainties in the context of alternative scenarios.

Downside risks to demand are more substantial than upside potential. There is a range of important drivers, in particular energy and environmental policies in consuming countries and technological developments, tending to reduce demand.

Uncertainties over future oil demand translate into a wide range of possible levels of necessary investment in OPEC Member Countries. Even over the medium-term to 2010, there is an estimated range of uncertainty of $50 billion for required investment in the upstream, increasing to $140 billion by 2015. This is part of why security of demand is a key concern for producers.

The expected increase in demand for oil products translates into a rising volume of crude that needs refining. Therefore, it is essential to focus attention upon the downstream sector as this is also a key element of the supply chain, and ultimately of market stability. In addition to rising demand, there is a continued move towards lighter and cleaner products. To meet this type of demand, the downstream sector will require significant investment to ensure that sufficient distillation capacity is in place, supported by adequate conversion, desulphurisation, as well as all other secondary processes and facilities.

The reference case for refining capacity expansion estimates that over 7 mb/d of new capacity — out of 14 mb/d of announced projects — will be added to the refining system globally by 2012. Almost 70% of the new capacity will be in the Middle East and Asia-Pacific. With capacity creep, the global reference case capacity additions from existing projects could reach just over 9 mb/d by 2015.

Other drivers of capacity creep

However, several factors will add to the downside risk in the reference case. Mainly because of rising downstream sector construction costs in recent years, combined with the difficulties in finding skilled labour and experienced professionals, these figures have the potential to change. This risk is further exacerbated by the reluctance of refiners to expedite the implementation of projects in light of the rapidly changing policies that put a strong emphasis on developing alternative fuels that compete directly with refined products.

These issues play out in the alternative cost-driven delayed scenario for short- and medium-term capacity expansion. In this scenario, the new distillation capacity additions could be reduced to as low as 8 mb/d for the period until 2015, including assumed capacity creep.

Recognising this, it is evident that up to 2010, refinery capacity expansion under the reference case for refinery projects just keeps pace with the required incremental refinery throughputs. The deficit is small, but does not indicate any potential easing of refinery capacity and utilisations in the shorter term. The cost-driven delayed scenario for capacity additions worsens the deficit.

Nevertheless, under the reference case outlook for refinery projects, the data indicates that capacity additions should exceed requirements in 2011 and 2012 as a range of new projects comes on stream, thereby easing refining tightness and potentially margins.

Under the cost-driven delayed scenario, the excess additions relative to reference requirements are essentially eliminated. Moreover, if global oil demand growth moves below reference case levels, then an easing in the refining sector could begin as early as 2008.

Uncertain projections for biofuels

There are uncertainties surrounding these projections. This is especially relevant for biofuels. In general, biofuels projects do not take as long to implement as refinery projects. The reference case allows for a significant medium-term increase in biofuels production. Any additional increase would further reduce required refinery throughputs and margins. Consequently, policy initiatives to support the development of biofuels may discourage refiners, as well as possibly crude oil producers, from investing in the needed capacity expansion.

Should such a situation be followed by biofuels failing to meet the stated targets, the result could be further tightness in the downstream, and possibly the upstream, and in turn, this could have a significant impact on prices, margins and volatility.

In any case, the Outlook states that under these circumstances, the follow-up question is whether refiners should hold sufficient spare capacity to cover potential losses. OPEC Member Countries have offered, and will continue to offer, an adequate level of upstream spare capacity for the benefit of the world at large.

Downstream investment in consuming nations

It is equally important, however, that adequate capacity also exists in the downstream sector at all times, which is primarily the responsibility of consuming nations.

Based on the reference case assessment of known projects, by 2015 a total of almost 2 mb/d of additional distillation capacity will be required, and by 2020, a further 3.7 mb/d. This is what is needed, on top of the assessed likely capacity additions, to bring the global refining system back into long-run balance, with refining margins that allow for a return on investment, but are not as tight as those of today.

Taking into account the most likely changes in the future supply and demand structures and their quality specifications, the global downstream sector will require in the period 2006–2020, 13 mb/d of additional distillation capacity, around 7.5 mb/d of combined upgrading capacity, 18 mb/d of desulphurisation capacity and 2 mb/d of capacity for other supporting processes, such as alkylation, isomerisation and reforming.

The total required investment in refinery processing to 2020 is projected to be $450 billion in the reference case. Of this, $110 billion comprises the cost of known projects, $110 billion covers the further required process unit additions and $230 billion comprises the ongoing maintenance and replacement. The Asia-Pacific requires the highest level of investment in new units to 2020, with China accounting for around 75% of the Asia-Pacific total.

Inter-regional oil trade should increase by 13 mb/d to almost 63 mb/d of oil exports in 2020. Both crude and products exports will increase appreciably, with products exports growing faster than crude oil exports. Correspondingly, the reference case outlook calls for a total tanker fleet requirement in 2020 of 460 million dwt. This compares to 360 million dwt as of the end of 2006.

Environmentally driven regulations also play an important role in respect to the refined products quality specifications. Clearly, this trend is set to continue in the future, creating a potential for market fragmentation unless regulations are introduced in a co-ordinated manner. Therefore, future quality regulations should, as much as possible, ensure the fungibility of fuels to avoid shortages and prevent unnecessary volatility in product and crude oil markets.

References:

OPEC: World Oil Outlook 2007 [*.pdf].

OPEC: OPEC releases its 2007 World Oil Outlook - June 26, 2007.

Most importantly, according to the report, the demand for OPEC crude by 2010 has been revised downwards and will be almost 1 million barrels per day (mb/d) below 2005 levels because of the rise of non-OPEC non-conventional resources (including biofuels) (click to enlarge). Thereafter, demand for OPEC oil will gradually increase. But uncertainties over demand, driven by the rise of green fuels and non-conventional resources, may have serious consequences and delay much needed investments across the entire supply chain. Especially the addition of new oil refinery capacity may get delayed.

Most importantly, according to the report, the demand for OPEC crude by 2010 has been revised downwards and will be almost 1 million barrels per day (mb/d) below 2005 levels because of the rise of non-OPEC non-conventional resources (including biofuels) (click to enlarge). Thereafter, demand for OPEC oil will gradually increase. But uncertainties over demand, driven by the rise of green fuels and non-conventional resources, may have serious consequences and delay much needed investments across the entire supply chain. Especially the addition of new oil refinery capacity may get delayed.In general, biofuels projects do not take as long to implement as refinery projects. The reference case allows for a significant medium-term increase in biofuels production. Any additional increase would further reduce required refinery throughputs and margins. Consequently, policy initiatives to support the development of biofuels may discourage refiners, as well as possibly crude oil producers, from investing in the needed capacity expansion.The result of this scenario is high fuel product and crude oil prices, expected to remain at a level of $50-60 per barrel until 2030. This is exactly the price bracket at which biofuels made in the South (e.g. sugarcane ethanol and palm oil biodiesel) can directly, without subsidies, compete with oil.

However, if the ambitious biofuel targets in the OECD are not met, the result could be further tightness in the downstream, and possibly the upstream, and in turn, this could have a significant impact on prices, margins and volatility. Such an event would automatically kickstart biofuel production again.

Global outlook

According to the report demand for energy in general is set to continue to grow (click to enlarge) and oil is expected to maintain its leading position in meeting the world’s growing energy needs for the foreseeable future. In OPEC's reference case, with an average global economic growth rate of 3.5% per annum (purchasing power parity basis), and oil prices assumed to remain in the $50-60/b range in nominal terms for much of the projection period, oil demand is set to rise from the 2005 level of 83 mb/d to 118 mb/d by 2030.

According to the report demand for energy in general is set to continue to grow (click to enlarge) and oil is expected to maintain its leading position in meeting the world’s growing energy needs for the foreseeable future. In OPEC's reference case, with an average global economic growth rate of 3.5% per annum (purchasing power parity basis), and oil prices assumed to remain in the $50-60/b range in nominal terms for much of the projection period, oil demand is set to rise from the 2005 level of 83 mb/d to 118 mb/d by 2030.This assumes that no particular departure in trends for energy policies and technologies takes place. This is a very important caveat for there are inherent downside risks to demand, something that is specifically addressed in the Outlook. One of these 'risks', is indeed the fast growth of biofuels and non-OPEC, non-conventional oil resources.

OECD countries, currently accounting for close to 60% of world oil demand, see a further growth of 4 mb/d by 2030, reaching 53 mb/d - mainly coming from North America. Developing countries account for most of the rise in the reference case, with consumption doubling from 29 mb/d to 58 mb/d. Asian developing countries account for an increase of 20 mb/d, which represents more than two-thirds of the growth in all developing countries.

Nevertheless, the Outlook assumes that energy poverty will remain an important issue over this period. By 2030, developing countries will consume, on average, approximately five times less oil per person, compared with OECD countries.

Demand per sector

The transportation sector will be the main source of future oil demand increases. Growth in the OECD is expected to continue to rise, although saturation effects should increasingly have an impact upon the growth in passenger car ownership. The potential for growth in the stock of cars, buses and lorries, however, is far greater in developing countries (click to enlarge). For example, two-thirds of the world’s population currently live in countries with less than one car per 20 people. The total stock of cars is expected to rise from 700 million in 2005 to 1.2 billion by 2030, and the global volume of commercial vehicles is anticipated to more than double: biofuels :: energy :: sustainability :: ethanol :: biodiesel :: biomass :: petroleum :: oil :: OPEC ::

The transportation sector will be the main source of future oil demand increases. Growth in the OECD is expected to continue to rise, although saturation effects should increasingly have an impact upon the growth in passenger car ownership. The potential for growth in the stock of cars, buses and lorries, however, is far greater in developing countries (click to enlarge). For example, two-thirds of the world’s population currently live in countries with less than one car per 20 people. The total stock of cars is expected to rise from 700 million in 2005 to 1.2 billion by 2030, and the global volume of commercial vehicles is anticipated to more than double: biofuels :: energy :: sustainability :: ethanol :: biodiesel :: biomass :: petroleum :: oil :: OPEC :: Of the non-transportation oil use, the main expected source of increase will be in

the industrial and residential sectors of developing countries, which see a combined

growth to 2030 of over 11 mboe/d in the reference case. Oil use in households is closely associated with the gradual switch away from traditional fuels. This trend is expected to continue, especially in the poorer developing countries of Asia and Africa, with the urbanisation movement throughout the developing world central to the shift towards commercial energy.

Despite the expected continued growth in electricity production and consumption, oil demand in this sector will experience no significant growth.

No 'Peak Oil', Non-OPEC production plateau

Resources are sufficient to meet future demand. Estimates from the US Geological

Survey of ultimately recoverable reserves have doubled since the early 1980s, while

cumulative production during this period was less than one-third of this increase.

This has been due to such factors as technology, successful exploration and enhanced

recovery from existing fields. On top of this, there is a vast resource base of nonconventional oil to explore and develop.

Non-OPEC crude oil supply at first rises in the reference case to a plateau of around 48 mb/d, before beginning a gradual decline from around 2020. This plateau is initially maintained as increases from Latin America (chiefly Brazil), Russia and the Caspian compensate for decreases elsewhere, mainly in the North Sea. The Middle East

and Africa region experiences a slight rise in volumes over the medium-term to 2010,

but this reaches a plateau of close to 5 mb/d. Non-OPEC crude oil supply is expected

to be just over 45 mb/d in 2030.

Biofuels, non-conventional oil

Regarding non-conventional oil supply and biofuels from non-OPEC countries, the most significant growth is expected to come from the Canadian oil sands, which is seen rising in the reference case to 5 mb/d in 2030, from just 1 mb/d in 2005. Coal-to- liquids and gas-to-liquids are also expected to grow, from about 150,000 b/d and less than 50,000 b/d, to 1.5 mb/d and 500,000 b/d respectively from 2005–2030. These increases will come predominantly from the US, China, South Africa and Australia.

The use of biofuels is also increasing in many regions throughout the world, and recent pronouncements of ambitious targets amplify uncertainties for future demand and supply volumes. In total, the reference case sees more than 10 mb/d of nonconventional oil supply including biofuels coming from non-OPEC by 2030, 8 mb/d more than in 2005.

Of those 10 mb/d, the bulk may come from biofuels, under a high scenario:

OPEC’s projections for biofuels supply in a high scenario case, which assumes an accelerated policy push in consuming countries, sees biofuels supply at just over 5 mb/d in 2030, thus realising even lower demand for oil products in general, and for OPEC oil in particular.

Uncertainty over the magnitude of the rise in non-OPEC non-conventional supply is growing. For example, the European Union recently adopted a minimum binding target for biofuels to reach a 10% share in transport gasoline and diesel consumption.

Uncertainty over the magnitude of the rise in non-OPEC non-conventional supply is growing. For example, the European Union recently adopted a minimum binding target for biofuels to reach a 10% share in transport gasoline and diesel consumption.And in the US, the most recent proposal, as reflected in the ‘Twenty In Ten Goal’, proposes alternative transport fuels hitting over 2 mb/d by 2017.

The Outlook's reference scenario for biofuel supply is extremely conservative (click to enlarge) compared to projections by other organisations (such as the IEA) or to the cumulative supply that would emerge if actual targets set by countries are met. But even in this reference case, OPEC sees the rise of biofuels as an important factor in the uncertainty over OPEC oil demand.

Demand for OPEC crude falls, stabilize, falls

Initial increases in both crude and non-crude supply pushes total non-OPEC supply up to 54 mb/d in 2010. This is 5 mb/d higher than in 2005. With demand rising by only a slightly higher rate, this leaves little room for additional OPEC oil. Indeed, with OPEC non-crude supply, primarily natural gas liquids (NGLs), set to rise to just under 6 mb/d by 2010, the demand for OPEC crude by 2010 is almost 1 mb/d below 2005 levels.

After 2010, non-OPEC crude supply, including NGLs, stabilises, then eventually falls. Yet with non-conventional oil supply increasing at strong rates, over the entire projection period, total non-OPEC supply actually continues to rise. The amount of

crude oil supply expected from OPEC increases post-2010, rising, in this reference case, to 38 mb/d by 2020 and 49 mb/d by 2030.

Investments in capacity

These projections underline the need for substantial investment along the entire supply chain. Expansion of non-OPEC capacity is two-to-three times more costly than in OPEC, with this gap widening over time. The highest cost region is the OECD, which also experiences the highest decline rates. Up to 2030, total upstream investment requirements, from 2006 onwards, amount to $2.4 trillion (in 2006 US$).

These estimates, however, do not include necessary infrastructure investments. Concerning crude oil price assumptions for medium- to long-term analyses, it has been observed that the oil industry, guided by the recent price trends, has mostly revised upward the business-as-usual price assumptions. A further observation is that, due to the effect of several factors, economic growth and oil demand are both now more resilient to higher oil prices than had previously been thought.

All these trends, in addition to rising costs, have become integral to the general perception of higher expected prices in the long-term. Continuous downward revisions to demand projections from organizations such as the International Energy Agency and the US Department of Energy/Energy Information Administration are also noted. In this regard, a key question is whether this downward revision process is set to continue.

On the supply side, there has been a steady rise in expectations for non-OPEC production in the longer term. Increased attention is being paid to non-conventional oil and biofuels and a discernibly higher expected contribution to supply is emerging.

Uncertainty over demand

There is a great deal of uncertainty over future demand and non-OPEC supply, which translates into large uncertainties over the amount of oil that OPEC Member Countries will eventually need to supply. Investment requirements are very large, and subject to considerably long lead-times and pay-back periods. It is therefore essential to explore these uncertainties in the context of alternative scenarios.

Downside risks to demand are more substantial than upside potential. There is a range of important drivers, in particular energy and environmental policies in consuming countries and technological developments, tending to reduce demand.

Uncertainties over future oil demand translate into a wide range of possible levels of necessary investment in OPEC Member Countries. Even over the medium-term to 2010, there is an estimated range of uncertainty of $50 billion for required investment in the upstream, increasing to $140 billion by 2015. This is part of why security of demand is a key concern for producers.

The expected increase in demand for oil products translates into a rising volume of crude that needs refining. Therefore, it is essential to focus attention upon the downstream sector as this is also a key element of the supply chain, and ultimately of market stability. In addition to rising demand, there is a continued move towards lighter and cleaner products. To meet this type of demand, the downstream sector will require significant investment to ensure that sufficient distillation capacity is in place, supported by adequate conversion, desulphurisation, as well as all other secondary processes and facilities.

The reference case for refining capacity expansion estimates that over 7 mb/d of new capacity — out of 14 mb/d of announced projects — will be added to the refining system globally by 2012. Almost 70% of the new capacity will be in the Middle East and Asia-Pacific. With capacity creep, the global reference case capacity additions from existing projects could reach just over 9 mb/d by 2015.

Other drivers of capacity creep

However, several factors will add to the downside risk in the reference case. Mainly because of rising downstream sector construction costs in recent years, combined with the difficulties in finding skilled labour and experienced professionals, these figures have the potential to change. This risk is further exacerbated by the reluctance of refiners to expedite the implementation of projects in light of the rapidly changing policies that put a strong emphasis on developing alternative fuels that compete directly with refined products.

These issues play out in the alternative cost-driven delayed scenario for short- and medium-term capacity expansion. In this scenario, the new distillation capacity additions could be reduced to as low as 8 mb/d for the period until 2015, including assumed capacity creep.

Recognising this, it is evident that up to 2010, refinery capacity expansion under the reference case for refinery projects just keeps pace with the required incremental refinery throughputs. The deficit is small, but does not indicate any potential easing of refinery capacity and utilisations in the shorter term. The cost-driven delayed scenario for capacity additions worsens the deficit.

Nevertheless, under the reference case outlook for refinery projects, the data indicates that capacity additions should exceed requirements in 2011 and 2012 as a range of new projects comes on stream, thereby easing refining tightness and potentially margins.

Under the cost-driven delayed scenario, the excess additions relative to reference requirements are essentially eliminated. Moreover, if global oil demand growth moves below reference case levels, then an easing in the refining sector could begin as early as 2008.

Uncertain projections for biofuels

There are uncertainties surrounding these projections. This is especially relevant for biofuels. In general, biofuels projects do not take as long to implement as refinery projects. The reference case allows for a significant medium-term increase in biofuels production. Any additional increase would further reduce required refinery throughputs and margins. Consequently, policy initiatives to support the development of biofuels may discourage refiners, as well as possibly crude oil producers, from investing in the needed capacity expansion.

Should such a situation be followed by biofuels failing to meet the stated targets, the result could be further tightness in the downstream, and possibly the upstream, and in turn, this could have a significant impact on prices, margins and volatility.

Biofuels also raises issues over the future structure of a complex downstream sector that includes both oil and biofuels. The question is how the sector should be structured in order to withstand major disruptions. With the increasing number of biofuel producers, the chances of losing this capacity for a longer period and over a larger area, for example due to drought, could easily lead to a shortage of required fuels.Let us remark that OPEC forgets that biofuels are being and will produced in many different countries and regions - projects can be planned and energy crops grown virtually anywhere, unlike oil which has to be 'discovered' - , so a local drought will only marginally affect global supply. A terrorist attack on one big oil refinery, a pipeline, or a major well would have much more impact.

In any case, the Outlook states that under these circumstances, the follow-up question is whether refiners should hold sufficient spare capacity to cover potential losses. OPEC Member Countries have offered, and will continue to offer, an adequate level of upstream spare capacity for the benefit of the world at large.

Downstream investment in consuming nations

It is equally important, however, that adequate capacity also exists in the downstream sector at all times, which is primarily the responsibility of consuming nations.

Based on the reference case assessment of known projects, by 2015 a total of almost 2 mb/d of additional distillation capacity will be required, and by 2020, a further 3.7 mb/d. This is what is needed, on top of the assessed likely capacity additions, to bring the global refining system back into long-run balance, with refining margins that allow for a return on investment, but are not as tight as those of today.

Taking into account the most likely changes in the future supply and demand structures and their quality specifications, the global downstream sector will require in the period 2006–2020, 13 mb/d of additional distillation capacity, around 7.5 mb/d of combined upgrading capacity, 18 mb/d of desulphurisation capacity and 2 mb/d of capacity for other supporting processes, such as alkylation, isomerisation and reforming.

The total required investment in refinery processing to 2020 is projected to be $450 billion in the reference case. Of this, $110 billion comprises the cost of known projects, $110 billion covers the further required process unit additions and $230 billion comprises the ongoing maintenance and replacement. The Asia-Pacific requires the highest level of investment in new units to 2020, with China accounting for around 75% of the Asia-Pacific total.

Inter-regional oil trade should increase by 13 mb/d to almost 63 mb/d of oil exports in 2020. Both crude and products exports will increase appreciably, with products exports growing faster than crude oil exports. Correspondingly, the reference case outlook calls for a total tanker fleet requirement in 2020 of 460 million dwt. This compares to 360 million dwt as of the end of 2006.

Environmentally driven regulations also play an important role in respect to the refined products quality specifications. Clearly, this trend is set to continue in the future, creating a potential for market fragmentation unless regulations are introduced in a co-ordinated manner. Therefore, future quality regulations should, as much as possible, ensure the fungibility of fuels to avoid shortages and prevent unnecessary volatility in product and crude oil markets.

References:

OPEC: World Oil Outlook 2007 [*.pdf].

OPEC: OPEC releases its 2007 World Oil Outlook - June 26, 2007.

0 Comments:

Post a Comment

Links to this post:

Create a Link

<< Home