IPCC Fourth Assessment Report: Mitigation

May 4, 2007

The following is an html version of the Summary for Policymakers of the IPCC Fourth Assessment Report, Working Group III. The original PDF version is here

A. Introduction

B. Greenhouse gas emission trends

C. Mitigation in the short and medium term (until 2030)

D. Mitigation in the long term (after 2030)

E. Policies, measures and instruments to mitigate climate change

F. Sustainable development and climate change mitigation

G. Gaps in knowledge

Endbox 1: Uncertainty representation

A. Introduction

1. The Working Group III contribution to the IPCC Fourth Assessment Report (AR4) focuses on new literature on the scientific, technological, environmental, economic and social aspects of mitigation of climate change, published since the IPCC Third Assessment Report (TAR) and the Special Reports on CO2 Capture and Storage (SRCCS) and on Safeguarding the Ozone Layer and the Global Climate System (SROC).

The following summary is organised into five sections after this introduction:

-

Greenhouse gas (GHG) emission trends

-

Mitigation in the short and medium term, across different economic sectors (until 2030)

-

Mitigation in the long-term (beyond 2030)

-

Policies, measures and instruments to mitigate climate change

-

Sustainable development and climate change mitigation.

References to the corresponding chapter sections are indicated at each paragraph in square brackets. An explanation of terms, acronyms and chemical symbols used in this SPM can be found in the glossary to the main report.

B. Greenhouse gas emission trends

2. Global greenhouse gas (GHG) emissions have grown since pre-industrial times, with an increase of 70% between 1970 and 2004 (high agreement, much evidence)

1

.

-

Since pre-industrial times, increasing emissions of GHGs due to human activities have led to a marked increase in atmospheric GHG concentrations [1.3; Working Group I SPM].

-

Between 1970 and 2004, global emissions of CO2, CH4, N2O, HFCs, PFCs and SF6, weighted by their global warming potential (GWP), have increased by 70% (24% between 1990 and 2004), from 28.7 to 49 Gigatonnes of carbon dioxide equivalents (GtCO2-eq)

2

(see Figure SPM.1). The emissions of these gases have increased at different rates. CO2 emissions have grown between 1970 and 2004 by about 80% (28% between 1990 and 2004) and represented 77% of total anthropogenic GHG emissions in 2004.

-

The largest growth in global GHG emissions between 1970 and 2004 has come from the energy supply sector (an increase of 145%). The growth in direct emissions

3

in this period from transport was 120%, industry 65% and land use, land use change, and forestry (LULUCF)

4

40%

5

. Between 1970 and 1990 direct emissions from agriculture grew by 27% and from buildings by 26%, and the latter remained at approximately at 1990 levels thereafter. However, the buildings sector has a high level of electricity use and hence the total of direct and indirect emissions in this sector is much higher (75%) than direct emissions [1.3, 6.1, 11.3, Figures 1.1 and 1.3].

-

The effect on global emissions of the decrease in global energy intensity (-33%) during 1970 to 2004 has been smaller than the combined effect of global income growth (77 %) and global population growth (69%); both drivers of increasing energy-related CO2 emissions (Figure SPM.2). The long-term trend of a declining carbon intensity of energy supply reversed after 2000. Differences in terms of per capita income, per capita emissions, and energy intensity among countries remain significant. (Figure SPM.3). In 2004 UNFCCC Annex I countries held a 20% share in world population, produced 57% of world Gross Domestic Product based on Purchasing Power Parity (GDPppp)

6

, and accounted for 46% of global GHG emissions (Figure SPM.3a) [1.3].

-

The emissions of ozone depleting substances (ODS) controlled under the Montreal Protocol

7

, which are also GHGs, have declined significantly since the 1990s. By 2004 the emissions of these gases were about 20% of their 1990 level [1.3].

-

A range of policies, including those on climate change, energy security

8

, and sustainable development, have been effective in reducing GHG emissions in different sectors and many countries. The scale of such measures, however, has not yet been large enough to counteract the global growth in emissions [1.3, 12.2].

-

3. With current climate change mitigation policies and related sustainable development practices, global GHG emissions will continue to grow over the next few decades (high agreement, much evidence).

-

The SRES (non-mitigation) scenarios project an increase of baseline global GHG emissions by a range of 9.7 GtCO2-eq to 36.7 GtCO2-eq (25-90%) between 2000 and 2030

9

(Box SPM.1 and Figure SPM.4). In these scenarios, fossil fuels are projected to maintain their dominant position in the global energy mix to 2030 and beyond. Hence CO2 emissions between 2000 and 2030 from energy use are projected to grow 45 to 110% over that period. Two thirds to three quarters of this increase in energy CO2 emissions is projected to come from non-Annex I regions, with their average per capita energy CO2 emissions being projected to remain substantially lower (2.8-5.1 tCO2/cap) than those in Annex I regions (9.6-15.1 tCO2/cap) by 2030. According to SRES scenarios, their economies are projected to have a lower energy use per unit of GDP (6.2 — 9.9 MJ/US$ GDP) than that of non-Annex I countries (11.0 — 21.6 MJ/US$ GDP). [1.3, 3.2]

[2000 and 2004 bars will be placed closer to reflect the smaller period between the years]

[Representation of note references will be improved]

Figure SPM 1: Global Warming Potential (GWP) weighted global greenhouse gas emissions 1970-2004. 100 year GWPs from IPCC 1996 (SAR) were used to convert emissions to CO2-eq. (cf. UNFCCC reporting guidelines). CO2, CH4, N2O, HFCs, PFCs and SF6 from all sources are included.

1)

2)

4)5)

3)

Gt CGt CGtCO2-eq/yr

6)

7)

The two CO2 emission categories reflect CO2 emissions from energy production and use (second from bottom) and from land use changes (third from the bottom) [Figure 1.1a].

Notes:

1. Other N2O includes industrial processes, deforestation/savannah burning, waste water and waste incineration.

2. Other is CH4 from industrial processes and savannah burning.

3. CO2 emissions from decay (decomposition) of above ground biomass that remains after logging and deforestation and CO2 from peat fires and decay of drained peat soils.

4. As well as traditional biomass use at 10% of total, assuming 90% is from sustainable biomass production. Corrected for 10% carbon of biomass that is assumed to remain as charcoal after combustion.

5. For large-scale forest and scrubland biomass burning averaged data for 1997-2002 based on Global Fire Emissions Data base satellite data.

6. Cement production and natural gas flaring.

7. Fossil fuel use includes emissions from feedstocks.

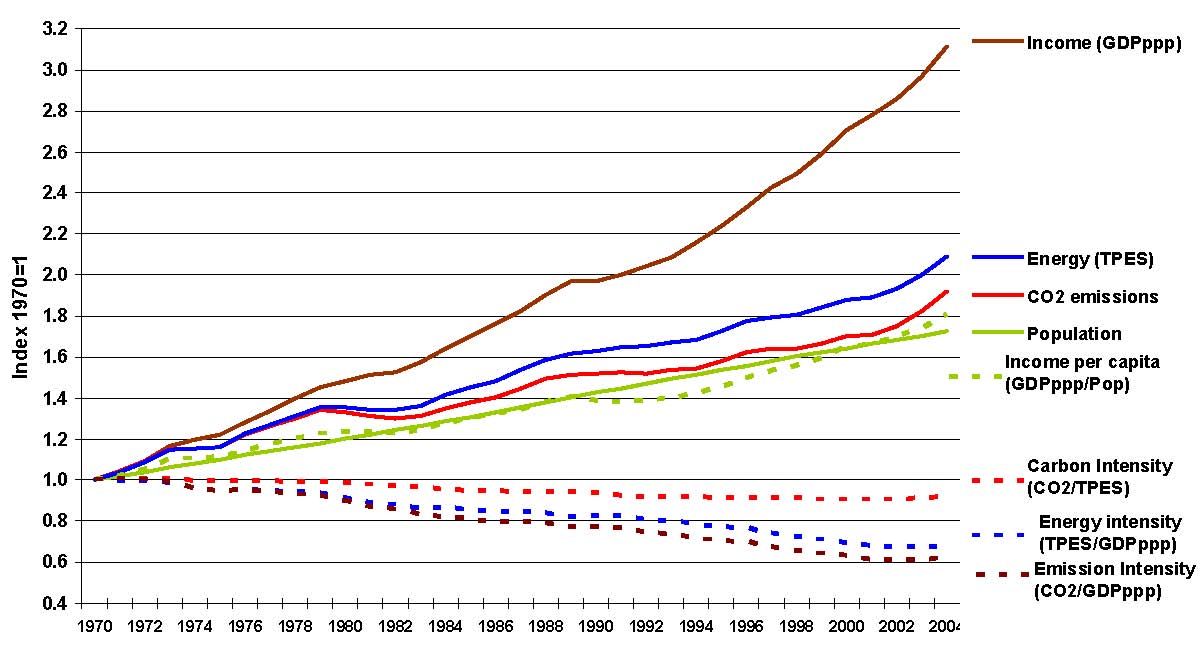

Figure SPM 2: Relative global development of Gross Domestic Product measured in PPP (GDPppp), Total Primary Energy Supply (TPES), CO2 emissions (from fossil fuel burning, gas flaring and cement manufacturing) and Population (Pop). In addition, in dotted lines, the figure shows Income per capita (GDPppp/Pop), Energy Intensity (TPES/GDPppp), Carbon Intensity of energy supply (CO2/TPES), and Emission Intensity of the economic production process (CO2/GDPppp) for the period 1970-2004. [Figure 1.5]

Figure SPM 3a: Year 2004 distribution of regional per capita GHG emissions (all Kyoto gases, including those from land-use) over the population of different country groupings. The percentages in the bars indicate a regions share in global GHG emissions [Figure 1.4a].

|

Figure SPM 3b: Year 2004 distribution of regional GHG emissions (all Kyoto gases, including those from land-use) per US$ of GDPppp over the GDPppp of different country groupings. The percentages in the bars indicate a regions share in global GHG emissions [Figure 1.4b].

|

[Authors will clarify country groupings in TS and chapter 1 figures; improve the editorial representation (enlarge) of the figure, including allowing for b/w printing]

[Include title above figures]

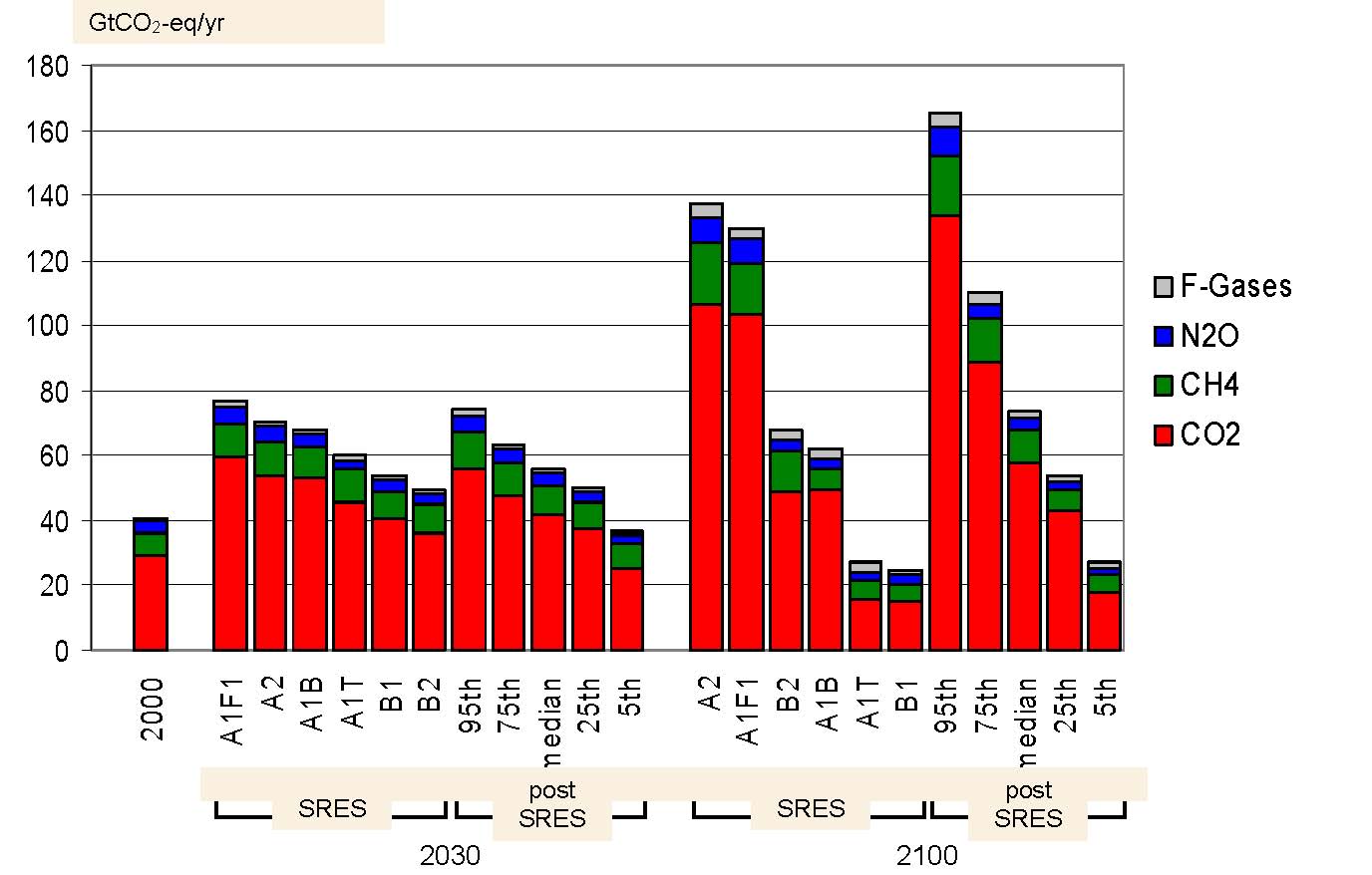

Figure SPM 4: Global GHG emissions for 2000 and projected baseline emissions for 2030 and 2100 from IPCC SRES and the post-SRES literature. The figure provides the emissions from the six illustrative SRES scenarios. It also provides the frequency distribution of the emissions in the post-SRES scenarios (5th, 25th, median, 75th, 95th percentile), as covered in chapter 3. F-gases cover HFCs, PFCs and SF6 [1.3, 3.2, Figure 1.7].

-

4. Baseline emissions scenarios published since SRES

10

, are comparable in range to those presented in the IPCC Special Report on Emission Scenarios (SRES) (25- 135 GtCO2-eq/yr in 2100, see Figure SPM.4). (high agreement, much evidence)

-

Studies since SRES used lower values for some drivers for emissions, notably population projections. However, for those studies incorporating these new population projections, changes in other drivers, such as economic growth, resulted in little change in overall emission levels. Economic growth projections for Africa, Latin America and the Middle East to 2030 in post-SRES baseline scenarios are lower than in SRES, but this has only minor effects on global economic growth and overall emissions [3.2].

-

Representation of aerosol and aerosol precursor emissions, including sulphur dioxide, black carbon, and organic carbon, which have a net cooling effect

11

has improved. Generally, they are projected to be lower than reported in SRES [3.2].

-

Available studies indicate that the choice of exchange rate for GDP (MER or PPP) does not appreciably affect the projected emissions, when used consistently

12

. The differences, if any, are small compared to the uncertainties caused by assumptions on other parameters in the scenarios, e.g. technological change [3.2].

Box SPM.1: The emission scenarios of the IPCC Special Report on Emission Scenarios (SRES)

A1. The A1 storyline and scenario family describes a future world of very rapid economic growth, global population that peaks in mid-century and declines thereafter, and the rapid introduction of new and more efficient technologies. Major underlying themes are convergence among regions, capacity building and increased cultural and social interactions, with a substantial reduction in regional differences in per capita income. The A1 scenario family develops into three groups that describe alternative directions of technological change in the energy system. The three A1 groups are distinguished by their technological emphasis: fossil intensive (A1FI), non fossil energy sources (A1T), or a balance across all sources (A1B) (where balanced is defined as not relying too heavily on one particular energy source, on the assumption that similar improvement rates apply to all energy supply and end use technologies).

A2. The A2 storyline and scenario family describes a very heterogeneous world. The underlying theme is self reliance and preservation of local identities. Fertility patterns across regions converge very slowly, which results in continuously increasing population. Economic development is primarily regionally oriented and per capita economic growth and technological change more fragmented and slower than other storylines.

B1. The B1 storyline and scenario family describes a convergent world with the same global population, that peaks in mid-century and declines thereafter, as in the A1 storyline, but with rapid change in economic structures toward a service and information economy, with reductions in material intensity and the introduction of clean and resource efficient technologies. The emphasis is on global solutions to economic, social and environmental sustainability, including improved equity, but without additional climate initiatives.

B2. The B2 storyline and scenario family describes a world in which the emphasis is on local solutions to economic, social and environmental sustainability. It is a world with continuously increasing global population, at a rate lower than A2, intermediate levels of economic development, and less rapid and more diverse technological change than in the B1 and A1 storylines. While the scenario is also oriented towards environmental protection and social equity, it focuses on local and regional levels.

An illustrative scenario was chosen for each of the six scenario groups A1B, A1FI, A1T, A2, B1 and B2. All should be considered equally sound.

The SRES scenarios do not include additional climate initiatives, which means that no scenarios are included that explicitly assume implementation of the United Nations Framework Convention on Climate Change or the emissions targets of the Kyoto Protocol.

This box summarizing the SRES scenarios is taken from the Third Assessment Report and has been subject to prior line by line approval by the Panel.

C. Mitigation in the short and medium term (until 2030)

Box SPM 2: Mitigation potential and analytical approaches

The concept of “mitigation potential” has been developed to assess the scale of GHG reductions that could be made, relative to emission baselines, for a given level of carbon price (expressed in cost per unit of carbon dioxide equivalent emissions avoided or reduced). Mitigation potential is further differentiated in terms of “market potential” and “economic potential”.

Market potential is the mitigation potential based on private costs and private discount rates

13

, which might be expected to occur under forecast market conditions, including policies and measures currently in place, noting that barriers limit actual uptake [2.4].

Economic potential is the mitigation potential, which takes into account social costs and benefits and social discount rates

14

, assuming that market efficiency is improved by policies and measures and barriers are removed [2.4].

Studies of market potential can be used to inform policy makers about mitigation potential with existing policies and barriers, while studies of economic potentials show what might be achieved if appropriate new and additional policies were put into place to remove barriers and include social costs and benefits. The economic potential is therefore generally greater than the market potential.

Mitigation potential is estimated using different types of approaches. There are two broad classes — “bottom-up” and “top-down” approaches, which primarily have been used to assess the economic potential.

Bottom-up studies are based on assessment of mitigation options, emphasizing specific technologies and regulations. They are typically sectoral studies taking the macro-economy as unchanged. Sector estimates have been aggregated, as in the TAR, to provide an estimate of global mitigation potential for this assessment.

Top-down studies assess the economy-wide potential of mitigation options. They use globally consistent frameworks and aggregated information about mitigation options and capture macro-economic and market feedbacks.

Bottom-up and top-down models have become more similar since the TAR as top-down models have incorporated more technological mitigation options and bottom-up models have incorporated more macroeconomic and market feedbacks as well as adopting barrier analysis into their model structures.

Bottom-up studies in particular are useful for the assessment of specific policy options at sectoral level, e.g. options for improving energy efficiency, while top-down studies are useful for assessing cross-sectoral and economy-wide climate change policies, such as carbon taxes and stabilization policies.

However, current bottom-up and top-down studies of economic potential have limitations in considering life-style choices, and in including all externalities such as local air pollution. They have limited representation of some regions, countries, sectors, gases, and barriers. The projected mitigation costs do not take into account potential benefits of avoided climate change.

|

Box SPM 3: Assumptions in studies on mitigation portfolios and macro-economic costs

Studies on mitigation portfolios and macro-economic costs assessed in this report are based on top-down modelling. Most models use a global least cost approach to mitigation portfolios and with universal emissions trading, assuming transparent markets, no transaction cost, and thus perfect implementation of mitigation measures throughout the 21st century. Costs are given for a specific point in time.

Global modelled costs will increase if some regions, sectors (e.g. land-use), options or gases are excluded. Global modelled costs will decrease with lower baselines, use of revenues from carbon taxes and auctioned permits, and if induced technological learning is included. These models do not consider climate benefits and generally also co-benefits of mitigation measures, or equity issues.

|

-

5. Both bottom-up and top-down studies indicate that there is substantial economic potential for the mitigation of global GHG emissions over the coming decades, that could offset the projected growth of global emissions or reduce emissions below current levels (high agreement, much evidence).

Uncertainties in the estimates are shown as ranges in the tables below to reflect the ranges of baselines, rates of technological change and other factors that are specific to the different approaches. Furthermore, uncertainties also arise from the limited information for global coverage of countries, sectors and gases.

Bottom-up studies:

-

In 2030, the economic potential estimated for this assessment from bottom-up approaches (see Box SPM.2) is presented in Table SPM 1 below and Figure SPM 5A. For reference: emissions in 2000 were equal to 43 GtCO2-eq. [11.3]:

Table SPM 1: Global economic mitigation potential in 2030 estimated from bottom-up studies.

Carbon price

(US$/tCO2-eq)

|

Economic mitigation potential

(GtCO2-eq/yr)

|

Reduction relative to SRES A1 B

(68 GtCO2- eq/yr)

%

|

Reduction

relative to

SRES B2

(49 GtCO2- eq/yr)

%

|

0

|

5-7

|

7-10

|

10-14

|

20

|

9-17

|

14-25

|

19-35

|

50

|

13-26

|

20-38

|

27-52

|

100

|

16-31

|

23-46

|

32-63

|

-

Studies suggest that mitigation opportunities with net negative costs

15

have the potential to reduce emissions by around 6 GtCO2-eq/yr in 2030. Realizing these requires dealing with implementation barriers [11.3].

-

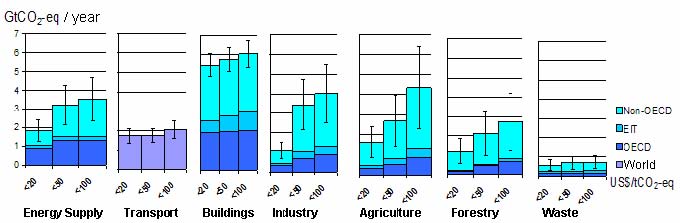

No one sector or technology can address the entire mitigation challenge. All assessed sectors contribute to the total (see Figure SPM 6). The technologies with the largest economic potential for the respective sectors are shown in Table SPM.3 [4.3, 4.4, 5.4, 6.5, 7.5, 8.4, 9.4, 10.4].

Top-down studies:

-

Top-down studies calculate an emission reduction for 2030 as presented in Table SPM 2 below and Figure SPM 5B. The global economic potentials found in the top-down studies are in line with bottom-up studies (see Box SPM 2), though there are considerable differences at the sectoral level [3.6].

Table SPM.2: Global economic potential in 2030 estimated from top-down studies.

Carbon price

(US$/tCO2-eq)

|

Economic potential

(GtCO2-eq/yr)

|

Reduction relative to

SRES A1 B

(68 GtCO2 eq/yr)

%

|

Reduction

relative to

SRES B2

(49 GtCO2 eq/yr)

%

|

20

|

9-18

|

13-27

|

18-37

|

50

|

14-23

|

21-34

|

29-47

|

100

|

17-26

|

25-38

|

35-53

|

-

The estimates in Table SPM 2 were derived from stabilization scenarios, i.e., runs towards long-run stabilization of atmospheric GHG concentration [3.6].

Figure SPM 5A:

Global economic potential in

2030 estimated from bottom-up studies

(data from Table SPM 1)

|

Figure SPM 5B:

Global economic potential in

2030 estimated from top-down studies

(data from Table SPM 2)

|

Table SPM 3: Key mitigation technologies and practices by sector. Sectors and technologies are listed in no particular order. Non-technological practices, such as lifestyle changes, which are cross-cutting, are not included in this table (but are addressed in paragraph 7 in this SPM).

Sector

|

Key mitigation technologies and practices currently commercially available.

|

Key mitigation technologies and practices projected to be commercialized before 2030.

|

Energy Supply

[4.3, 4.4]

|

Improved supply and distribution efficiency; fuel switching from coal to gas; nuclear power; renewable heat and power (hydropower, solar, wind, geothermal and bioenergy); combined heat and power; early applications of CCS (e.g. storage of removed CO2 from natural gas)

|

Carbon Capture and Storage (CCS) for gas, biomass and coal-fired electricity generating facilities; advanced nuclear power; advanced renewable energy, including tidal and waves energy, concentrating solar, and solar PV.

|

Transport

[5.4]

|

More fuel efficient vehicles; hybrid vehicles; cleaner diesel vehicles; biofuels; modal shifts from road transport to rail and public transport systems; non-motorised transport (cycling, walking); land-use and transport planning

|

Second generation biofuels; higher efficiency aircraft; advanced electric and hybrid vehicles with more powerful and reliable batteries

|

Buildings

[6.5]

|

Efficient lighting and daylighting; more efficient electrical appliances and heating and cooling devices; improved cook stoves, improved insulation ; passive and active solar design for heating and cooling; alternative refrigeration fluids, recovery and recycle of fluorinated gases

|

Integrated design of commercial buildings including technologies, such as intelligent meters that provide feedback and control; solar PV integrated in buildings

|

Industry

[7.5]

|

More efficient end-use electrical equipment; heat and power recovery; material recycling and substitution; control of non-CO2 gas emissions; and a wide array of process-specific technologies

|

Advanced energy efficiency; CCS for cement, ammonia, and iron manufacture; inert electrodes for aluminium manufacture

|

Agriculture

[8.4]

|

Improved crop and grazing land management to increase soil carbon storage; restoration of cultivated peaty soils and degraded lands; improved rice cultivation techniques and livestock and manure management to reduce CH4 emissions; improved nitrogen fertilizer application techniques to reduce N2O emissions; dedicated energy crops to replace fossil fuel use; improved energy efficiency

|

Improvements of crops yields

|

Forestry/forests [9.4]

|

Afforestation; reforestation; forest management; reduced deforestation; harvested wood product management; use of forestry products for bioenergy to replace fossil fuel use

|

Tree species improvement to increase biomass productivity and carbon sequestration. Improved remote sensing technologies for analysis of vegetation/ soil carbon sequestration potential and mapping land use change

|

Waste [10.4]

|

Landfill methane recovery; waste incineration with energy recovery; composting of organic waste; controlled waste water treatment; recycling and waste minimization

|

Biocovers and biofilters to optimize CH4 oxidation

|

(potential at <US$100/tCO2-eq: 2.4 – 4.7 Gt CO2-eq/yr)

|

(potential at <US$100/tCO2-eq: 1.6 – 2.5 Gt CO2-eq/yr)

|

(potential at <US$100/tCO2-eq: 5.3 -6.7

|

(potential at <US$100/tCO2-eq: 2.5 – 5.5 Gt CO2-eq/yr)

|

(potential at <US$100/tCO2-eq: 2.3 -6.4 Gt CO2-eq/yr)

|

(potential at <US$100/tCO2-eq: 1.3 – 4.2 Gt CO2-eq/yr)

|

(potential at <US$100/tCO2-eq: 0.4 – 1 Gt CO2-eq/yr)

|

Figure SPM 6: Estimated sectoral economic potential for global mitigation for different regions as a function of carbon price in 2030 from bottom-up studies, compared to the respective baselines assumed in the sector assessments. A full explanation of the derivation of this figure is found in 11.3.

Notes:

-

1. The ranges for global economic potentials as assessed in each sector are shown by vertical lines. The ranges are based on end-use allocations of emissions, meaning that emissions of electricity use are counted towards the end-use sectors and not to the energy supply sector.

-

2. The estimated potentials have been constrained by the availability of studies particularly at high carbon price levels.

-

3. . Sectors used different baselines. For industry the SRES B2 baseline was taken, for energy supply and transport the WEO 2004 baseline was used; the building sector is based on a baseline in between SRES B2 and A1B; for waste, SRES A1B driving forces were used to construct a waste specific baseline, agriculture and forestry used baselines that mostly used B2 driving forces.

-

4. Only global totals for transport are shown because international aviation is included [5.4].

-

5. Categories excluded are: non-CO2 emissions in buildings and transport, part of material efficiency options, heat production and cogeneration in energy supply, heavy duty vehicles, shipping and high-occupancy passenger transport, most high-cost options for buildings, wastewater treatment, emission reduction from coal mines and gas pipelines, fluorinated gases from energy supply and transport. The underestimation of the total economic potential from these emissions is of the order of 10-15%.

-

6. In 2030 macro-economic costs for multi-gas mitigation, consistent with emissions trajectories towards stabilization between 445 and 710 ppm CO2-eq, are estimated at between a 3% decrease of global GDP and a small increase, compared to the baseline (see Table SPM.4). However, regional costs may differ significantly from global averages (high agreement, medium evidence) (see Box SPM.3 for the methodologies and assumptions of these results).

-

The majority of studies conclude that reduction of GDP relative to the GDP baseline increases with the stringency of the stabilization target.

Table SPM.4: Estimated global macro-economic costs in 2030

16

for least-cost trajectories towards different long-term stabilization levels.

17

,

18

Stabilization levels (ppm CO2-eq)

|

Median

GDP reduction

19

(%)

|

Range of GDP reduction

19

,

20

(%)

|

Reduction of average annual GDP growth rates (percentage points)

19

,

21

|

590-710

|

0.2

|

-0.6 — 1.2

|

< 0.06

|

535-590

|

0.6

|

0.2 — 2.5

|

<0.1

|

445-535

22

|

Not available

|

< 3

|

< 0.12

|

-

Depending on the existing tax system and spending of the revenues, modelling studies indicate that costs may be substantially lower under the assumption that revenues from carbon taxes or auctioned permits under an emission trading system are used to promote low-carbon technologies or reform of existing taxes [11.4].

-

Studies that assume the possibility that climate change policy induces enhanced technological change also give lower costs. However, this may require higher upfront investment in order to achieve costs reductions thereafter [3.3, 3.4, 11.4, 11.5, 11.6].

-

Although most models show GDP losses, some show GDP gains because they assume that baselines are non-optimal and mitigation policies improve market efficiencies, or they assume that more technological change may be induced by mitigation policies. Examples of market inefficiencies include unemployed resources, distortionary taxes and/or subsidies [3.3, 11.4].

-

A multi-gas approach and inclusion of carbon sinks generally reduces costs substantially compared to CO2 emission abatement only.

-

Regional costs are largely dependent on the assumed stabilization level and baseline scenario. The allocation regime is also important, but for most countries to a lesser extent than the stabilization level [11.4, 13.3].

-

7. Changes in lifestyle and behaviour patterns can contribute to climate change mitigation across all sectors. Management practices can also have a positive role. (high agreement, medium evidence)

-

Lifestyle changes can reduce GHG emissions. Changes in lifestyles and consumption patterns that emphasize resource conservation can contribute to developing a low-carbon economy that is both equitable and sustainable [4.1, 6.7].

-

Education and training programmes can help overcome barriers to the market acceptance of energy efficiency, particularly in combination with other measures [Table 6.6].

-

Changes in occupant behaviour, cultural patterns and consumer choice and use of technologies can result in considerable reduction in CO2 emissions related to energy use in buildings [6.7].

-

Transport Demand Management, which includes urban planning (that can reduce the demand for travel) and provision of information and educational techniques (that can reduce car usage and lead to an efficient driving style) can support GHG mitigation [5.1].

-

In industry, management tools that include staff training, reward systems, regular feedback, documentation of existing practices can help overcome industrial organization barriers, reduce energy use, and GHG emissions [7.3].

-

8. While studies use different methodologies, in all analyzed world regions near-term health co-benefits from reduced air pollution as a result of actions to reduce GHG emissions can be substantial and may offset a substantial fraction of mitigation costs (high agreement, much evidence).

-

Including co-benefits other than health, such as increased energy security, and increased agricultural production and reduced pressure on natural ecosystems, due to decreased tropospheric ozone concentrations, would further enhance cost savings [11.8].

-

Integrating air pollution abatement and climate change mitigation policies offers potentially large cost reductions compared to treating those policies in isolation [11.8].

-

-

9. Literature since TAR confirms that there may be effects from Annex I countries action on the global economy and global emissions, although the scale of carbon leakage remains uncertain (high agreement, medium evidence).

-

Fossil fuel exporting nations (in both Annex I and non-Annex I countries) may expect, as indicated in TAR

23

, lower demand and prices and lower GDP growth due to mitigation policies. The extent of this spill over

24

depends strongly on assumptions related to policy decisions and oil market conditions [11.7].

-

Critical uncertainties remain in the assessment of carbon leakage

25

. Most equilibrium modelling support the conclusion in the TAR of economy-wide leakage from Kyoto action in the order of 5-20%, which would be less if competitive low-emissions technologies were effectively diffused [11.7] .

-

10. New energy infrastructure investments in developing countries, upgrades of energy infrastructure in industrialized countries, and policies that promote energy security, can, in many cases, create opportunities to achieve GHG emission reductions compared to baseline scenarios. Additional co-benefits are country-specific but often include air pollution abatement, balance of trade improvement, provision of modern energy services to rural areas and employment (high agreement, much evidence).

-

Future energy infrastructure investment decisions, expected to total over 20 trillion US$

26

between now and 2030, will have long term impacts on GHG emissions, because of the long life-times of energy plants and other infrastructure capital stock. The widespread diffusion of low-carbon technologies may take many decades, even if early investments in these technologies are made attractive. Initial estimates show that returning global energy-related CO2 emissions to 2005 levels by 2030 would require a large shift in the pattern of investment, although the net additional investment required ranges from negligible to 5-10% [4.1, 4.4, 11.6].

-

It is often more cost-effective to invest in end-use energy efficiency improvement than in increasing energy supply to satisfy demand for energy services. Efficiency improvement has a positive effect on energy security, local and regional air pollution abatement, and employment [4.2, 4.3, 6.5, 7.7, 11.3, 11.8].

-

Renewable energy generally has a positive effect on energy security, employment and on air quality. Given costs relative to other supply options, renewable electricity, which accounted for 18% of the electricity supply in 2005, can have a 30-35% share of the total electricity supply in 2030 at carbon prices up to 50 US$/tCO2-eq [4.3, 4.4, 11.3, 11.6, 11.8].

-

The higher the market prices of fossil fuels, the more low-carbon alternatives will be competitive, although price volatility will be a disincentive for investors. Higher priced conventional oil resources, on the other hand, may be replaced by high carbon alternatives such as from oil sands, oil shales, heavy oils, and synthetic fuels from coal and gas, leading to increasing GHG emissions, unless production plants are equipped with CCS [4.2, 4.3, 4.4, 4.5].

-

Given costs relative to other supply options, nuclear power, which accounted for 16% of the electricity supply in 2005, can have an 18% share of the total electricity supply in 2030 at carbon prices up to 50 US$/tCO2-eq, but safety, weapons proliferation and waste remain as constraints [4.2, 4.3, 4.4]

27

.

-

CCS in underground geological formations is a new technology with the potential to make an important contribution to mitigation by 2030. Technical, economic and regulatory developments will affect the actual contribution [4.3, 4.4].

-

11. There are multiple mitigation options in the transport sector

28

, but their effect may be counteracted by growth in the sector. Mitigation options are faced with many barriers, such as consumer preferences and lack of policy frameworks (medium agreement, medium evidence).

-

Improved vehicle efficiency measures, leading to fuel savings, in many cases have net benefits (at least for light-duty vehicles), but the market potential is much lower than the economic potential due to the influence of other consumer considerations, such as performance and size. There is not enough information to assess the mitigation potential for heavy-duty vehicles. Market forces alone, including rising fuel costs, are therefore not expected to lead to significant emission reductions [5.3, 5.4].

-

Biofuels might play an important role in addressing GHG emissions in the transport sector, depending on their production pathway. Biofuels used as gasoline and diesel fuel additives/substitutes are projected to grow to 3% of total transport energy demand in the baseline in 2030. This could increase to about 5-10%, depending on future oil and carbon prices, improvements in vehicle efficiency and the success of technologies to utilise cellulose biomass [5.3, 5.4].

-

Modal shifts from road to rail and inland waterway shipping and from low-occupancy to high-occupancy passenger transportation

29

, as well as land-use, urban planning and non-motorized transport offer opportunities for GHG mitigation, depending on local conditions and policies [5.3, 5.5].

-

Medium term mitigation potential for CO2 emissions from the aviation sector can come from improved fuel efficiency, which can be achieved through a variety of means, including technology, operations and air traffic management. However, such improvements are expected to only partially offset the growth of aviation emissions. Total mitigation potential in the sector would also need to account for non-CO2 climate impacts of aviation emissions [5.3, 5.4].

-

Realizing emissions reductions in the transport sector is often a co-benefit of addressing traffic congestion, air quality and energy security [5.5].

-

12. Energy efficiency options for new and existing buildings could considerably reduce CO2 emissions with net economic benefit. Many barriers exist against tapping this potential, but there are also large co-benefits (high agreement, much evidence).

-

By 2030, about 30% of the projected GHG emissions in the building sector can be avoided with net economic benefit [6.4, 6.5].

-

Energy efficient buildings, while limiting the growth of CO2 emissions, can also improve indoor and outdoor air quality, improve social welfare and enhance energy security [6.6, 6.7].

-

Opportunities for realising GHG reductions in the building sector exist worldwide. However, multiple barriers make it difficult to realise this potential. These barriers include availability of technology, financing, poverty, higher costs of reliable information, limitations inherent in building designs and an appropriate portfolio of policies and programs [6.7, 6.8].

-

The magnitude of the above barriers is higher in the developing countries and this makes it more difficult for them to achieve the GHG reduction potential of the building sector [6.7].

-

13. The economic potential in the industrial sector is predominantly located in energy intensive industries. Full use of available mitigation options is not being made in either industrialized or developing nations (high agreement, much evidence).

-

Many industrial facilities in developing countries are new and include the latest technology with the lowest specific emissions. However, many older, inefficient facilities remain in both industrialized and developing countries. Upgrading these facilities can deliver significant emission reductions [7.1, 7.3, 7.4].

-

The slow rate of capital stock turnover, lack of financial and technical resources, and limitations in the ability of firms, particularly small and medium-sized enterprises, to access and absorb technological information are key barriers to full use of available mitigation options [7.6].

-

14. Agricultural practices collectively can make a significant contribution at low cost to increasing soil carbon sinks, to GHG emission reductions, and by contributing biomass feedstocks for energy use (medium agreement, medium evidence).

-

A large proportion of the mitigation potential of agriculture (excluding bioenergy) arises from soil carbon sequestration, which has strong synergies with sustainable agriculture and generally reduces vulnerability to climate change [8.4, 8.5, 8.8].

-

Stored soil carbon may be vulnerable to loss through both land management change and climate change [8.10].

-

Considerable mitigation potential is also available from reductions in methane and nitrous oxide emissions in some agricultural systems [8.4, 8.5].

-

There is no universally applicable list of mitigation practices; practices need to be evaluated for individual agricultural systems and settings [8.4].

Biomass from agricultural residues and dedicated energy crops can be an important bioenergy feedstock, but its contribution to mitigation depends on demand for bioenergy from transport and energy supply, on water availability, and on requirements of land for food and fibre production. Widespread use of agricultural land for biomass production for energy may compete with other land uses and can have positive and negative environmental impacts and implications for food security [8.4, 8.8].

-

15. Forest-related mitigation activities can considerably reduce emissions from sources and increase CO2 removals by sinks at low costs, and can be designed to create synergies with adaptation and sustainable development (high agreement, much evidence)

30

.

-

About 65% of the total mitigation potential (up to 100 US$/tCO2-eq) is located in the tropics and about 50% of the total could be achieved by reducing emissions from deforestation [9.4].

-

Climate change can affect the mitigation potential of the forest sector (i.e., native and planted forests) and is expected to be different for different regions and sub-regions, both in magnitude and direction [9.5].

-

Forest-related mitigation options can be designed and implemented to be compatible with adaptation, and can have substantial co-benefits in terms of employment, income generation, biodiversity and watershed conservation, renewable energy supply and poverty alleviation [9.5, 9.6, 9.7].

-

16. Post-consumer waste

31

is a small contributor to global GHG emissions

32

(<5%), but the waste sector can positively contribute to GHG mitigation at low cost and promote sustainable development (high agreement, much evidence).

-

Existing waste management practices can provide effective mitigation of GHG emissions from this sector: a wide range of mature, environmentally effective technologies are commercially available to mitigate emissions and provide co-benefits for improved public health and safety, soil protection and pollution prevention, and local energy supply [10.3, 10.4, 10.5].

-

Waste minimization and recycling provide important indirect mitigation benefits through the conservation of energy and materials [10.4].

-

Lack of local capital is a key constraint for waste and wastewater management in developing countries and countries with economies in transition. Lack of expertise on sustainable technology is also an important barrier [10.6].

-

17. Geo-engineering options, such as ocean fertilization to remove CO2 directly from the atmosphere, or blocking sunlight by bringing material into the upper atmosphere, remain largely speculative and unproven, and with the risk of unknown side-effects. Reliable cost estimates for these options have not been published (medium agreement, limited evidence) [11.2].

D. Mitigation in the long term (after 2030)

-

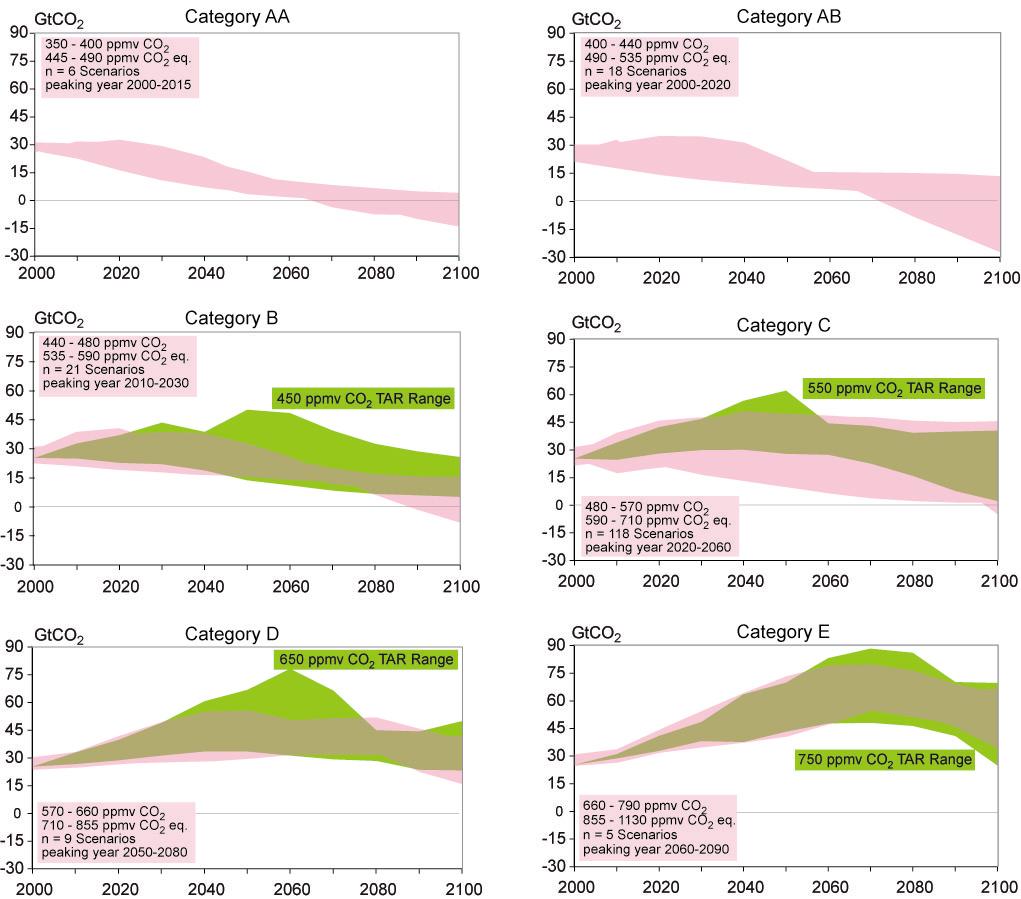

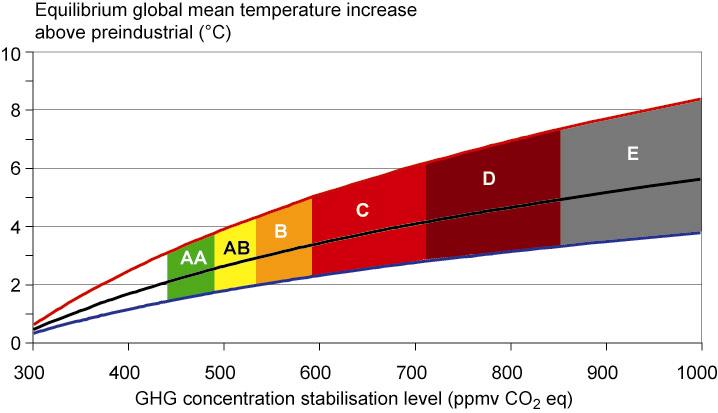

18. In order to stabilize the concentration of GHGs in the atmosphere, emissions would need to peak and decline thereafter. The lower the stabilization level, the more quickly this peak and decline would need to occur. Mitigation efforts over the next two to three decades will have a large impact on opportunities to achieve lower stabilization levels (see Table SPM.5, and Figure SPM. 8)

33

(high agreement, much evidence).

-

Recent studies using multi-gas reduction have explored lower stabilization levels than reported in TAR.

-

Assessed studies contain a range of emissions profiles for achieving stabilization of GHG concentrations

34

. Most of these studies used a least cost approach and include both early and delayed emission reductions (Figure SPM.7) [Box SPM 2]. Table SPM.5 summarizes the required emissions levels for different groups of stabilization concentrations and the associated equilibrium global mean temperature increase

35

, using the best estimate’ of climate sensitivity (see also Figure SPM.8 for the likely range of uncertainty)

36

. Stabilization at lower concentration and related equilibrium temperature levels advances the date when emissions need to peak, and requires greater emissions reductions by 2050.

Table SPM.5: Characteristics of post-TAR stabatiscenarios [Table TS 2, 3.10]

37

Category

|

Radiative

Forcing

|

CO2

Concentration

|

CO2-eq

Concentration

|

ilizon Global mean temperature increase above pre-industrial at equilibrium, using “best estimate” climate sensitivity

38

,

39

|

Peaking year for CO2 emissions

40

|

Change in global CO2 emissions in 2050 (% of 2000 emissions)

|

No. of assessed scenarios

|

|

W/m2

|

ppm

|

ppm

|

ºC

|

Year

|

percent

|

|

A1

|

2.5 — 3.0

|

350 — 400

|

445 — 490

|

2.0 — 2.4

|

2000 – 2015

|

-85 to -50

|

6

|

A2

|

3.0 — 3.5

|

400 — 440

|

490 — 535

|

2.4 — 2.8

|

2000 – 2020

|

-60 to -30

|

18

|

B

|

3.5 — 4.0

|

440 — 485

|

535 — 590

|

2.8 — 3.2

|

2010 – 2030

|

-30 to +5

|

21

|

C

|

4.0 — 5.0

|

485 — 570

|

590 — 710

|

3.2 — 4.0

|

2020 – 2060

|

+10 to +60

|

118

|

D

|

5.0 — 6.0

|

570 — 660

|

710 — 855

|

4.0 — 4.9

|

2050 – 2080

|

+25 to +85

|

9

|

E

|

6.0 — 7.5

|

660 — 790

|

855 — 1130

|

4.9 — 6.1

|

2060 – 2090

|

+90 to +140

|

5

|

Total

|

|

|

|

|

|

177

|

Median

|

GDP reduction

43

(%)

|

Range of GDP reduction

43

,

44

|

(%)

|

|

590-710

|

0.5

|

-1 — 2

|

|

535-590

|

1.3

|

slightly negative — 4

|

[Editorial Note: In the column titled “Category”, A1, A2, B

, will be changed to Roman numerals (I, II, III

)]

[Categories will be changed to I to VI; ppmv will be replaced with ppm; GtCO2 needs to GtCO2 / year]

Figure SPM 7: Emissions pathways of mitigation scenarios for alternative categories of stabilization levels (Category I to VI as defined in the box in each panel). The pathways are for CO2 emissions only. Pink shaded (dark) areas give the CO2 emissions for the post-TAR emissions scenarios. Green shaded (light) areas depict the range of more than 80 TAR stabilization scenarios. Base year emissions may differ between models due to differences in sector and industry coverage. To reach the lower stabilization levels some scenarios deploy removal of CO2 from the atmosphere (negative emissions) using technologies such as biomass energy production utilizing carbon capture and storage. [Figure 3.17]

[Capital letters will be changed from AA, AB etc into I to VI; ppmv (x-axis) will be changed to ppm; stabilisation in stabilization]

Figure SPM 8: Stabilization scenario categories as reported in Figure SPM.7 (coloured bands) and their relationship to equilibrium global mean temperature change above pre-industrial, using (i) “best estimate” climate sensitivity of 3°C (black line in middle of shaded area), (ii) upper bound of likely range of climate sensitivity of 4.5°C (red line at top of shaded area) (iii) lower bound of likely range of climate sensitivity of 2°C (blue line at bottom of shaded area). Coloured shading shows the concentration bands for stabilization of greenhouse gases in the atmosphere corresponding to the stabilization scenario categories I to VI as indicated in Figure SPM.7. The data are drawn from AR4 WGI, Chapter 10.8.

-

19. The range of stabilization levels assessed can be achieved by deployment of a portfolio of technologies that are currently available and those that are expected to be commercialised in coming decades. This assumes that appropriate and effective incentives are in place for development, acquisition, deployment and diffusion of technologies and for addressing related barriers (high agreement, much evidence).

-

The contribution of different technologies to emission reductions required for stabilization will vary over time, region and stabilization level.

-

o Energy efficiency plays a key role across many scenarios for most regions and timescales.

-

o For lower stabilization levels, scenarios put more emphasis on the use of low-carbon energy sources, such as renewable energy and nuclear power, and the use of CO2 capture and storage (CCS). In these scenarios improvements of carbon intensity of energy supply and the whole economy need to be much faster than in the past.

-

o Including non-CO2 and CO2 land-use and forestry mitigation options provides greater flexibility and cost-effectiveness for achieving stabilization. Modern bioenergy could contribute substantially to the share of renewable energy in the mitigation portfolio.

-

o For illustrative examples of portfolios of mitigation options, see figure SPM.9 [3.3, 3.4].

-

Investments in and world-wide deployment of low-GHG emission technologies as well as technology improvements through public and private Research, Development & Demonstration (RD&D) would be required for achieving stabilization targets as well as cost reduction. The lower the stabilization levels, especially those of 550 ppm CO2-eq or lower, the greater the need for more efficient RD&D efforts and investment in new technologies during the next few decades.

-

Appropriate incentives could address these barriers and help realize the goals across a wide portfolio of technologies. This requires that barriers to development, acquisition, deployment and diffusion of technologies are effectively addressed. [2.7, 3.3, 3.4, 3.6, 4.3, 4.4, 4.6].

-

[In figure, “and avoided deforestation” will be removed]

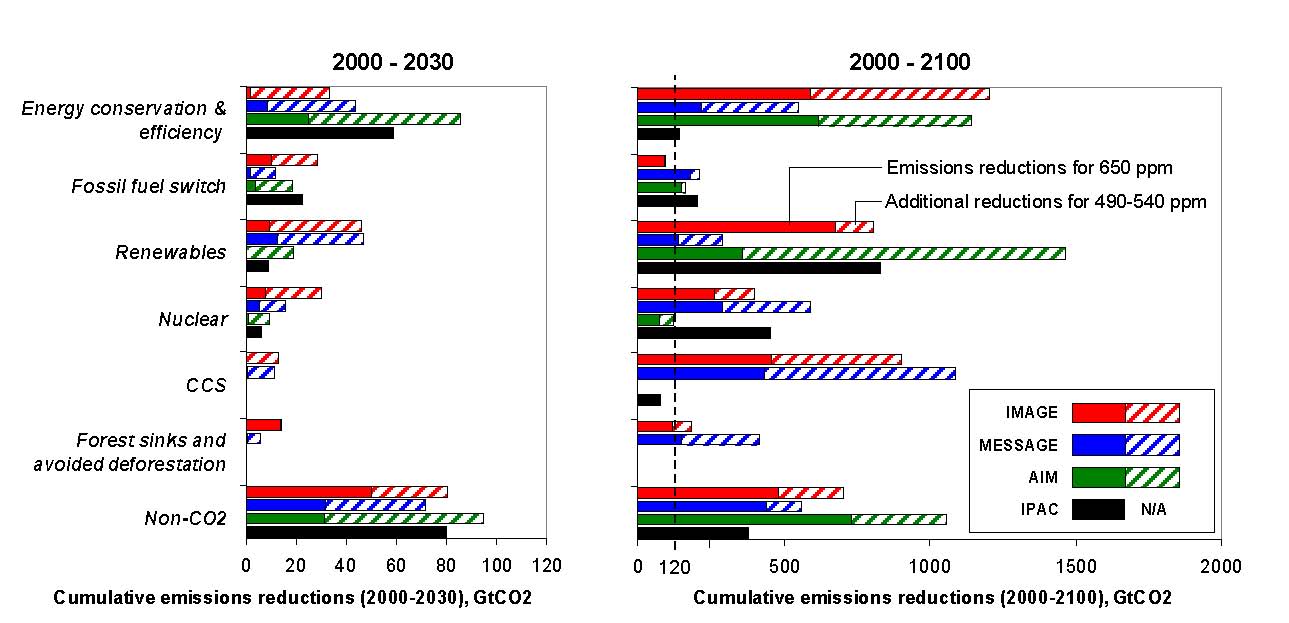

Figure SPM 9: Cumulative emissions reductions for alternative mitigation measures for 2000 to 2030 (left-hand panel) and for 2000-2100 (right-hand panel). The figure shows illustrative scenarios from four models (AIM, IMAGE, IPAC and MESSAGE) aiming at the stabilization at 490-540 ppm CO2-eq and levels of 650 ppm CO2-eq, respectively. Dark bars denote reductions for a target of 650 ppm CO2-eq and light bars the additional reductions to achieve 490-540 ppm CO2-eq. Note that some models do not consider mitigation through forest sink enhancement (AIM and IPAC) or CCS (AIM) and that the share of low-carbon energy options in total energy supply is also determined by inclusion of these options in the baseline. CCS includes carbon capture and storage from biomass. Forest sinks include reducing emissions from deforestation. [Figure 3.23]

-

20. In 2050

41

global average macro-economic costs for multi-gas mitigation towards stabilization between 710 and 445 ppm CO2-eq, are between a 1% gain to a 5.5% decrease of global GDP (see Table SPM.6). For specific countries and sectors, costs vary considerably from the global average. (See Box SPM.3 for the methodologies and assumptions and paragraph 5 for explanation of negative costs) (high agreement, medium evidence).

Table SPM.6: Estimated global macro-economic costs in 2050 relative to the baseline for least-cost trajectories towards different long-term stabilization targets

42

[3.3, 13.3]

Stabilization levels (ppm CO2-eq)

Reduction of average annual GDP growth rates (percentage points)

43

,

45

< 0.05

<0.1

-

445- 535

46

-

Not available

-

< 5.5

-

-

21. Decision-making about the appropriate level of global mitigation over time involves an iterative risk management process that includes mitigation and adaptation, taking into account actual and avoided climate change damages, co-benefits, sustainability, equity, and attitudes to risk. Choices about the scale and timing of GHG mitigation involve balancing the economic costs of more rapid emission reductions now against the corresponding medium-term and long-term climate risks of delay [high agreement, much evidence].

Limited and early analytical results from integrated analyses of the costs and benefits of mitigation indicate that these are broadly comparable in magnitude, but do not as yet permit an unambiguous determination of an emissions pathway or stabilization level where benefits exceed costs [3.5].

Integrated assessment of the economic costs and benefits of different mitigation pathways shows that the economically optimal timing and level of mitigation depends upon the uncertain shape and character of the assumed climate change damage cost curve. To illustrate this dependency:

o if the climate change damage cost curve grows slowly and regularly, and there is good foresight (which increases the potential for timely adaptation), later and less stringent mitigation is economically justified;

o alternatively if the damage cost curve increases steeply, or contains non-linearities (e.g. vulnerability thresholds or even small probabilities of catastrophic events), earlier and more stringent mitigation is economically justified [3.6].

Climate sensitivity is a key uncertainty for mitigation scenarios that aim to meet a specific temperature level. Studies show that if climate sensitivity is high then the timing and level of mitigation is earlier and more stringent than when it is low [3.5, 3.6].

Delayed emission reductions lead to investments that lock in more emission-intensive infrastructure and development pathways. This significantly constrains the opportunities to achieve lower stabilization levels (as shown in Table SPM.6) and increases the risk of more severe climate change impacts [3.4, 3.1, 3.5, 3.6]

Box SPM.4: Modelling induced technological change

23. Policies that provide a real or implicit price of carbon could create incentives for producers and consumers to significantly invest in low-GHG products, technologies and processes. Such policies could include economic instruments, government funding and regulation (high agreement, much evidence).

An effective carbon-price signal could realize significant mitigation potential in all sectors [11.3, 13.2].

Modelling studies (see Box SPM.3) show carbon prices rising to 20 to 80 US$/tCO2-eq by 2030 and 30 to 155 US$/tCO2-eq by 2050 are consistent with stabilization at around 550 ppm CO2-eq by 2100. For the same stabilization level, studies since TAR that take into account induced technological change lower these price ranges to 5 to 65 US$/tCO2eq in 2030 and 15 to 130 US$/tCO2-eq in 2050 [3.3, 11.4, 11.5].

|

Most top-down, as well as some 2050 bottom-up assessments, suggest that real or implicit carbon prices of 20 to 50 US$/tCO2-eq, sustained or increased over decades, could lead to a power generation sector with low-GHG emissions by 2050 and make many mitigation options in the end-use sectors economically attractive. [4.4,11.6]

Barriers to the implementation of mitigation options are manifold and vary by country and sector. They can be related to financial, technological, institutional, informational and behavioural aspects [4.5, 5.5, 6.7, 7.6, 8.6, 9.6, 10.5].

|

|

Table SPM.7: Selected sectoral policies, measures and instruments that have shown to be environmentally effective in the respective sector in at least a number of national cases.

|

Modelling studies (see Box SPM.3) show carbon prices rising to 20 to 80 US$/tCO2-eq by 2030 and 30 to 155 US$/tCO2-eq by 2050 are consistent with stabilization at around 550 ppm CO2-eq by 2100. For the same stabilization level, studies since TAR that take into account induced technological change lower these price ranges to 5 to 65 US$/tCO2eq in 2030 and 15 to 130 US$/tCO2-eq in 2050 [3.3, 11.4, 11.5].

|

Most top-down, as well as some 2050 bottom-up assessments, suggest that real or implicit carbon prices of 20 to 50 US$/tCO2-eq, sustained or increased over decades, could lead to a power generation sector with low-GHG emissions by 2050 and make many mitigation options in the end-use sectors economically attractive. [4.4,11.6]

Barriers to the implementation of mitigation options are manifold and vary by country and sector. They can be related to financial, technological, institutional, informational and behavioural aspects [4.5, 5.5, 6.7, 7.6, 8.6, 9.6, 10.5].

|

|

Table SPM.7: Selected sectoral policies, measures and instruments that have shown to be environmentally effective in the respective sector in at least a number of national cases.

|

Sector Sector

|

Policies

4747

, measures and instruments shown to be environmentally effective Policies, measures and instruments shown to be environmentally effective

|

Key constraints or opportunities Key constraints or opportunities

|

Energy supply [4.5]

|

Reduction of fossil fuel subsidies

|

Resistance by vested interests may make them difficult to implement

|

|

Taxes or carbon charges on fossil fuels

|

|

|

Feed-in tariffs for renewable energy technologies

|

May be appropriate to create markets for low emissions technologies

|

|

Renewable energy obligations

|

|

|

Producer subsidies

|

|

Transport [5.5]

|

Mandatory fuel economy, biofuel blending and CO2 standards for road transport

|

Partial coverage of vehicle fleet may limit effectiveness

|

|

Taxes on vehicle purchase, registration, use and motor fuels, road and parking pricing

|

Effectiveness may drop with higher incomes

|

|

Influence mobility needs through land use regulations, and infrastructure planning

|

Particularly appropriate for countries that are building up their transportation systems

|

|

Investment in attractive public transport facilities and non-motorised forms of transport

|

|

Buildings [6.8]

|

Appliance standards and labelling

|

Periodic revision of standards needed

|

|

Building codes and certification

|

Attractive for new buildings. Enforcement can be difficult

|

|

Demand-side management programmes

|

Need for regulations so that utilities may profit

|

|

Public sector leadership programmes, including procurement

|

Government purchasing can expand demand for energy-efficient products

|

|

Incentives for energy service companies (ESCOs)

|

Success factor: Access to third party financing

|

Industry [7.9]

|

Provision of benchmark information

|

May be appropriate to stimulate technology uptake. Stability of national policy important in view of international competitiveness

|

|

Performance standards

|

|

|

Subsidies, tax credits

|

|

|

Tradable permits

|

Predictable allocation mechanisms and stable price signals important for investments

|

|

Voluntary agreements

|

Success factors include: clear targets, a baseline scenario, third party involvement in design and review and formal provisions of monitoring, close cooperation between government and industry.

|

Agriculture [8.6, 8.7, 8.8]

|

Financial incentives and regulations for improved land management, maintaining soil carbon content, efficient use of fertilizers and irrigation

|

May encourage synergy with sustainable development and with reducing vulnerability to climate change, thereby overcoming barriers to implementation

|

Forestry/Forests [9.6]

|

Financial incentives (national and international) to increase forest area, to reduce deforestation, and to maintain and manage forests

|

Constraints include lack of investment capital and land tenure issues. Can help poverty alleviation.

|

|

Land use regulation and enforcement

|

|

Waste management [10.5]

|

Financial incentives for improved waste and wastewater management

|

May stimulate technology diffusion

|

|

Renewable energy incentives or obligations

|

Local availability of low-cost fuel

|

|

Waste management regulations

|

Most effectively applied at national level with enforcement strategies

|

-

24. Government support through financial contributions, tax credits, standard setting and market creation is important for effective technology development, innovation and deployment. Transfer of technology to developing countries depends on enabling conditions and financing (high agreement, much evidence).

-

Public benefits of RD&D investments are bigger than the benefits captured by the private sector, justifying government support of RD&D.

-

Government funding in real absolute terms for most energy research programmes has been flat or declining for nearly two decades (even after the UNFCCC came into force) and is now about half of the 1980 level [2.7, 3.4, 4.5, 11.5, 13.2].

-

Governments have a crucial supportive role in providing appropriate enabling environment, such as, institutional, policy, legal and regulatory frameworks

48

, to sustain investment flows and for effective technology transfer — without which it may be difficult to achieve emission reductions at a significant scale. Mobilizing financing of incremental costs of low-carbon technologies is important. International technology agreements could strengthen the knowledge infrastructure [13.3].

-

The potential beneficial effect of technology transfer to developing countries brought about by Annex I countries action may be substantial, but no reliable estimates are available [11.7].

-

Financial flows to developing countries through CDM projects have the potential to reach levels of the order of several billions US$ per year

49

, which is higher than the flows through the Global Environment Facility (GEF), comparable to the energy oriented development assistance flows, but at least an order of magnitude lower than total foreign direct investment flows. The financial flows through CDM, GEF and development assistance for technology transfer have so far been limited and geographically unequally distributed [12.3, 13.3].

-

25. Notable achievements of the UNFCCC and its Kyoto protocol are the establishment of a global response to the climate problem, stimulation of an array of national policies, the creation of an international carbon market and the establishment of new institutional mechanisms that may provide the foundation for future mitigation efforts (high agreement, much evidence).

-

The impact of the protocol’s first commitment period relative to global emissions is projected to be limited. Its economic impacts on participating Annex-B countries are projected to be smaller than presented in TAR, that showed 0.2-2% lower GDP in 2012 without emissions trading, and 0.1-1.1% lower GDP with emissions trading among Annex-B countries [1.4, 11.4, 13.3].

-

26. The literature identifies many options for achieving reductions of global GHG emissions at the international level through cooperation. It also suggests that successful agreements are environmentally effective, cost-effective, incorporate distributional considerations and equity, and are institutionally feasible (high agreement, much evidence).

-

Greater cooperative efforts to reduce emissions will help to reduce global costs for achieving a given level of mitigation, or will improve environmental effectiveness [13.3].

-

Improving, and expanding the scope of, market mechanisms (such as emission trading, Joint Implementation and CDM) could reduce overall mitigation costs [13.3].

-

Efforts to address climate change can include diverse elements such as emissions targets; sectoral, local, sub-national and regional actions; RD&D programmes; adopting common policies; implementing development oriented actions; or expanding financing instruments. These elements can be implemented in an integrated fashion, but comparing the efforts made by different countries quantitatively would be complex and resource intensive [13.3].

-

Actions that could be taken by participating countries can be differentiated both in terms of when such action is undertaken, who participates and what the action will be. Actions can be binding or non-binding, include fixed or dynamic targets, and participation can be static or vary over time [13.3].

F. Sustainable development and climate change mitigation

-

27. Making development more sustainable by changing development paths can make a major contribution to climate change mitigation, but implementation may require resources to overcome multiple barriers. There is a growing understanding of the possibilities to choose and implement mitigation options in several sectors to realize synergies and avoid conflicts with other dimensions of sustainable development (high agreement, much evidence).

-

Irrespective of the scale of mitigation measures, adaptation measures are necessary [1.2].

-

Addressing climate change can be considered an integral element of sustainable development policies. National circumstances and the strengths of institutions determine how development policies impact GHG emissions. Changes in development paths emerge from the interactions of public and private decision processes involving government, business and civil society, many of which are not traditionally considered as climate policy. This process is most effective when actors participate equitably and decentralized decision making processes are coordinated [2.2, 3.3, 12.2].

-

Climate change and other sustainable development policies are often but not always synergistic. There is growing evidence that decisions about macroeconomic policy, agricultural policy, multilateral development bank lending, insurance practices, electricity market reform, energy security and forest conservation, for example, which are often treated as being apart from climate policy, can significantly reduce emissions. On the other hand, decisions about improving rural access to modern energy sources for example may not have much influence on global GHG emissions [12.2].

-

Climate change policies related to energy efficiency and renewable energy are often economically beneficial, improve energy security and reduce local pollutant emissions. Other energy supply mitigation options can be designed to also achieve sustainable development benefits such as avoided displacement of local populations, job creation, and health benefits [4.5,12.3].

-

Reducing both loss of natural habitat and deforestation can have significant biodiversity, soil and water conservation benefits, and can be implemented in a socially and economically sustainable manner. Forestation and bioenergy plantations can lead to restoration of degraded land, manage water runoff, retain soil carbon and benefit rural economies, but could compete with land for food production and may be negative for biodiversity, if not properly designed [9.7, 12.3].

-

There are also good possibilities for reinforcing sustainable development through mitigation actions in the waste management, transportation and buildings sectors [5.4, 6.6, 10.5, 12.3].

-

Making development more sustainable can enhance both mitigative and adaptive capacity, and reduce emissions and vulnerability to climate change. Synergies between mitigation and adaptation can exist, for example properly designed biomass production, formation of protected areas, land management, energy use in buildings and forestry. In other situations, there may be trade-offs, such as increased GHG emissions due to increased consumption of energy related to adaptive responses [2.5, 3.5, 4.5, 6.9, 7.8, 8.5, 9.5, 11.9, 12.1].

G. Gaps in knowledge

-

28. There are still relevant gaps in currently available knowledge regarding some aspects of mitigation of climate change, especially in developing countries. Additional research addressing those gaps would further reduce uncertainties and thus facilitate decision-making related to mitigation of climate change [TS.14].

Endbox 1: Uncertainty representation

Uncertainty is an inherent feature of any assessment. The fourth assessment report clarifies the uncertainties associated with essential statements.

Fundamental differences between the underlying disciplinary sciences of the three Working Group reports make a common approach impractical. The “likelihood” approach applied in "Climate change 2007, the physical science basis" and the “confidence” and “likelihood” approaches used in "Climate change 2007, impacts, adaptation, and vulnerability" were judged to be inadequate to deal with the specific uncertainties involved in this mitigation report, as here human choices are considered.

In this report a two-dimensional scale is used for the treatment of uncertainty. The scale is based on the expert judgment of the authors of WGIII on the level of concurrence in the literature on a particular finding (level of agreement), and the number and quality of independent sources qualifying under the IPCC rules upon which the finding is based (amount of evidence

50

) (see Table SPM.E.1). This is not a quantitative approach, from which probabilities relating to uncertainty can be derived.

Table SPM E.1: Qualitative definition of uncertainty

|

High agreement,

limited evidence

|

High agreement,

medium evidence

|

High agreement,

much evidence

|

|

Medium agreement, limited evidence

|

Medium agreement,

medium evidence

|

Medium agreement,

much evidence

|

Level of agreement (on a particular finding)

|

Low agreement,

limited evidence

|

Low agreement,

medium evidence

|

Low agreement,

much evidence

|

|

Amount of evidence

50

(number and quality of independent sources)

|

Because the future is inherently uncertain, scenarios i.e. internally consistent images of different futures – not predictions of the future – have been used extensively in this report.

1 Each headline statement has an “agreement/evidence” assessment attached that is supported by the bullets underneath. This does not necessarily mean that this level of “agreement/evidence”applies to each bullet. Endbox 1 provides an explanation of this representation of uncertainty.

2 The definition of carbon dioxide equivalent (CO2-eq) is the amount of CO2 emission that would cause the same radiative forcing as an emitted amount of a well mixed greenhouse gas or a mixture of well mixed greenhouse gases, all multiplied with their respective GWPs to take into account the differing times they remain in the atmosphere [WGI AR4 Glossary].

3 Direct emissions in each sector do not include emissions from the electricity sector for the electricity consumed in the building, industry and agricultural sectors or of the emissions from refinery operations supplying fuel to the transport sector.

4 The term “land use, land use change and forestry” is used here to describe the aggregated emissions of CO2, CH4, N2O from deforestation, biomass and burning, decay of biomass from logging and deforestation, decay of peat and peat fires [1.3.1]. This is broader than emissions from deforestation, which is included as a subset. The emissions reported here do not include carbon uptake (removals).

5 This trend is for the total LULUCF emissions, of which emissions from deforestation are a subset and, owing to large data uncertainties, is significantly less certain than for other sectors. The rate of deforestation globally was slightly lower in the 2000-2005 period than in the 1990-2000 period [9.2.1].

6 The GDPppp metric is used for illustrative purposes only for this report. For an explanation of PPP and Market Exchange Rate (MER) GDP calculations, see footnote 12.

7 Halons, chlorofluorocarbons (CFCs), hydrochlorofluorocarbons (HCFCs), methyl chloroform (CH3CCl3), carbon tetrachloride (CCl4) and methyl bromide (CH3Br).

8 Energy security refers to security of energy supply.

9 The SRES 2000 GHG emissions assumed here are 39.8 GtCO2-eq, i.e. lower than the emissions reported in the EDGAR database for 2000 (45 GtCO2-eq). This is mostly due to differences in LULUCF emissions.

10 Baseline scenarios do not include additional climate policy above current ones; more recent studies differ with respect to UNFCCC and Kyoto Protocol inclusion.

11 see AR4 WG I report, chapter 10.2.

12 Since TAR, there has been a debate on the use of different exchange rates in emission scenarios. Two metrics are used to compare GDP between countries. Use of MER is preferable for analyses involving internationally traded products. Use of PPP, is preferable for analyses involving comparisons of income between countries at very different stages of development. Most of the monetary units in this report are expressed in MER. This reflects the large majority of emissions mitigation literature that is calibrated in MER. When monetary units are expressed in PPP, this is denoted by GDPppp.

13 Private costs and discount rates reflect the perspective of private consumers and companies; see Glossary for a fuller description.

14 Social costs and discount rates reflect the perspective of society. Social discount rates are lower than those used by private investors; see Glossary for a fuller description.

15 In this report, as in the SAR and the TAR, options with net negative costs (no regrets opportunities) are defined as those options whose benefits such as reduced energy costs and reduced emissions of local/regional pollutants equal or exceed their costs to society, excluding the benefits of avoided climate change (see Box SPM 1).

16 For a given stabilization level, GDP reduction would increase over time in most models after 2030. Long-term costs also become more uncertain. [Figure 3.25]

17 Results based on studies using various baselines.

18 Studies vary in terms of the point in time stabilization is achieved; generally this is in 2100 or later.

19 This is global GDP based market exchange rates.

20 The median and the 10th and 90th percentile range of the analyzed data are given.

21 The calculation of the reduction of the annual growth rate is based on the average reduction during the period till 2030 that would result in the indicated GDP decrease in 2030.

22 The number of studies that report GDP results is relatively small and they generally use low baselines.

23 See TAR WG III (2001) SPM paragraph 16.

24 Spill over effects of mitigation in a cross-sectoral perspective are the effects of mitigation policies and measures in one country or group of countries on sectors in other countries.

25 Carbon leakage is defined as the increase in CO2 emissions outside the countries taking domestic mitigation action divided by the reduction in the emissions of these countries.

26 20 trillion = 20000 billion= 20*1012.

27 Austria could not agree with this statement.

28 See Table SPM.1 and Figure SPM.6.

29 Including rail, road and marine mass transit and carpooling

30 Tuvalu noted difficulties with the reference to “low costs” as Chapter 9, page 15 of the WG III report states that: “the cost of forest mitigation projects rise significantly when opportunity costs of land are taken into account”.

31 Industrial waste is covered in the industry sector.

32 GHGs from waste include landfill and wastewater methane, wastewater N2O, and CO2 from incineration of fossil carbon.

33 Paragraph 2A addresses historical GHG emissions since pre-industrial times.

34 Studies vary in terms of the point in time stabilization is achieved; generally this is around 2100 or later.

35 The information on global mean temperature is taken from the AR4 WGI report, chapter 10.8. These temperatures are reached well after concentrations are stabilized.

36 The equilibrium climate sensitivity is a measure of the climate system response to sustained radiative forcing. It is not a projection but is defined as the global average surface warming following a doubling of carbon dioxide concentrations [AR4 WGI SPM].

37 The understanding of the climate system response to radiative forcing as well as feedbacks is assessed in detail in the AR4 WGI Report. Feedbacks between the carbon cycle and climate change affect the required mitigation for a particular stabilization level of atmospheric carbon dioxide concentration. These feedbacks are expected to increase the fraction of anthropogenic emissions that remains in the atmosphere as the climate system warms. Therefore, the emission reductions to meet a particular stabilization level reported in the mitigation studies assessed here might be underestimated.

38 The best estimate of climate sensitivity is 3ºC [WG 1 SPM].

39 Note that global mean temperature at equilibrium is different from expected global mean temperature at the time of stabilization of GHG concentrations due to the inertia of the climate system. For the majority of scenarios assessed, stabilisation of GHG concentrations occurs between 2100 and 2150.

40 Ranges correspond to the 15th to 85th percentile of the post-TAR scenario distribution. CO2 emissions are shown so multi-gas scenarios can be compared with CO2-only scenarios.

41 Cost estimates for 2030 are presented in paragraph 5.

42 This corresponds to the full literature across all baselines and mitigation scenarios that provide GDP numbers.